What’s next for Retail?

Diana Stafie is Foresight Strategist & Founder of Future Station, a consultancy practise focused on strategy building by using foresight methodology and tools. Understanding “How the Future of… might look like” is the core mission. Diana designs and runs Future Scenarios and Trends Scanning projects, Trends lectures and future-related keynotes.

What does the future hold for retail after the Covid19 pandemic?

What new consumer needs have emerged?

What innovations are brands considering?

I have recently collaborated with Retail Expert Vlad Ardeleanu on a foresight project aimed at developing scenarios for a post Covid19 reality. And below we have summarized some of our conclusions regarding the retail context.

Retail Expert Vlad Ardeleanu

Learn about foresight and scenario planning.

Retail sales surge to pre-Covid19 levels – a cause for optimism?

Covid19 pandemic has fundamentally changed the global retail landscape. Shopper behaviour has evolved and adapted with unprecedented speed. Today, shoppers are more selective and discerning in how they shop and what they buy.

Reading consumer behaviour was never easy. Today, deciphering the consumer looks more difficult than ever.

Consumer confidence and sales trends are always good indicators to start learning about retail status-quo. It is a good place to start in understanding metrics about consumer behaviour.

With 2019 confidence levels at historic high, it was only natural that Covid19 would rapidly erode confidence and send the index to historic lows.

Nielsen’s Global Consumer Confidence Index fell from 107 to 92 in 2020. And retail sales follow confidence levels. US retail sales fell 9% in March and 16% in April versus last year. The EU had similar patterns, with retail trade down 8% in March and 18% in April.

When the outlook is all bleak and global expert consensus forecasted retail sales decrease of 10% in 2020, a surprise happened. Sales surged back with unprecedented strength.

US and EU sales jumped back 18% in May. More growth followed in June with 8% in the US and 5% in the EU. Retail spending in July topped pre-pandemic levels announced by both the US and EU.

Asian countries made similar announcements. After all the panic and close parallels with the Great Depression (or other crisis), having till now only three negative months in retail sales is unexpected great news. Can this be a cause for optimism?

Retail innovation landscape

Here are 4 examples of how retail brands have adopted already to the new landscape:

1. Voice-based e-commerce grocery shopping experience (June 2020)

France-based Carrefour and Google launched voice-controlled grocery shopping for the grocery chain’s e-commerce platform. After connecting their Google and Carrefour accounts, shoppers can add items to their shopping list using voice commands via Google Assistant on their smartphone or other devices. More details here.

2. Free telenutrition service to promote healthy and affordable eating (May 2020)

Kroger Health offers telemedicine consultations to help consumers make healthier dietary choices. The service was launched in response to tightened consumer budgets and reduced availability of fresh produce due to the coronavirus. More details here.

3. Contact-free shopping and collection

Selver, an Estonian supermarket chain, launched a robotic grocery locker service allowing customers to collect online orders without human contact. With two temperature zones, the robot can safely store fresh and frozen items, offering convenient curbside pick up in various locations. More details here.

4. Smart shopping cart for cashier-less shopping (July 2020)

Amazon unveiled Dash Cart: a smart shopping cart that allows shoppers to skip checkout lines. To use the Dash Cart, shoppers scan an on-screen QR code with the Amazon app to verify their account. The cart uses built-in cameras and scales to detect items placed inside. More details here.

Future of Retail: implications

Consumers expect Covid19 period to be limited. Despite the drop in reported consumer confidence, we trust that consumers expect this Covid19 period to be brief.

The possible availability of a vaccine early next year could mean a return to normality in the next six to ten months. One argument in favour of this idea is that some of the important share price indexes are already back to pre-pandemic levels.

However, consumer shopping behaviour will never go back. If for volume levels we already see recovery, we cannot say the same about consumer shopping behaviours. The crisis has prompted a surge of new activities, with a good percentage of consumers trying new shopping behaviour in response to economic pressures, store closings, and changing priorities. But which of these changes will stick?

5 highly important changes we believe brands should consider

1. Low touch retail is here to stay

The low touch economy refers to the newly imposed restrictions and constraints that will dictate the direction of retail. As coined by the Board of Innovation, the idea of “low touch economy” pinpoints the drastic change in the way businesses will see more reliance on automation or robots to overtake repetitive tasks, regular cleaning in storefronts, and having employees work remotely.

2. E-commerce in the spotlight

While the shift to online shopping has been near-universal across categories, high-income earners and millennials are leading the way in shifting spend online across both essential and non-essential items.

A McKinsey study published in August 2020 found that consumers significantly intend to shop online even after the Covid19 crisis. There is a 10% average growth in customers purchasing online in each and every category.

Digital shopping is definitely here to stay, with categories such as over-the-counter medicine, groceries, household supplies and personal-care products to grow the fastest.

3. Affordability seekers

Some of the current changes in consumer behaviour will largely mirror the changes that manifested during the 2008 recession, yet on a shorter time-frame and with greater speed.

Most consumers today worry about the state of the economy, how long this crisis will last and overall health concerns. Population savings are growing everywhere in the world since consumers are increasingly looking for value and affordability in their spending.

4. Data-driven retail

Mastering data enables you to understand and manage operational activities, such as customer pickup options, customer profiles and product preferences.

Understanding each of these characteristics allows you to develop a 360-degree view of your customer — and better meet their needs. A great example here is the approach of UK-based retailer Sainsbury’s. Using data and analytics Sainsbury’s has designed its new locations in order to match the needs of busy city workers (more details here).

5. Brand loyalties are disrupted

Product availability has been top of mind for consumers as food manufacturers adjust to meet surging retail demand during early days of the COVID-19 pandemic. Empty shelves and temporary stock-outs have disrupted brand loyalty and generated increased trials of both national branded and private label grocery items.

Price sensitivity has also been a factor. Consumers have been more willing to try new private label brands than national brands. Shopping behaviour favouring convenience and proximity was another factor for brand loyalty.

A surprising upturn for the smaller convenience stores was registered, despite difficult sales in Q2 2020. This was first spotted in Asian markets and went on to become a world trend as reported by a recent Nielsen survey.

In light of economic uncertainty, consumers will continue shopping closer to home for a more diverse assortment of products and categories.

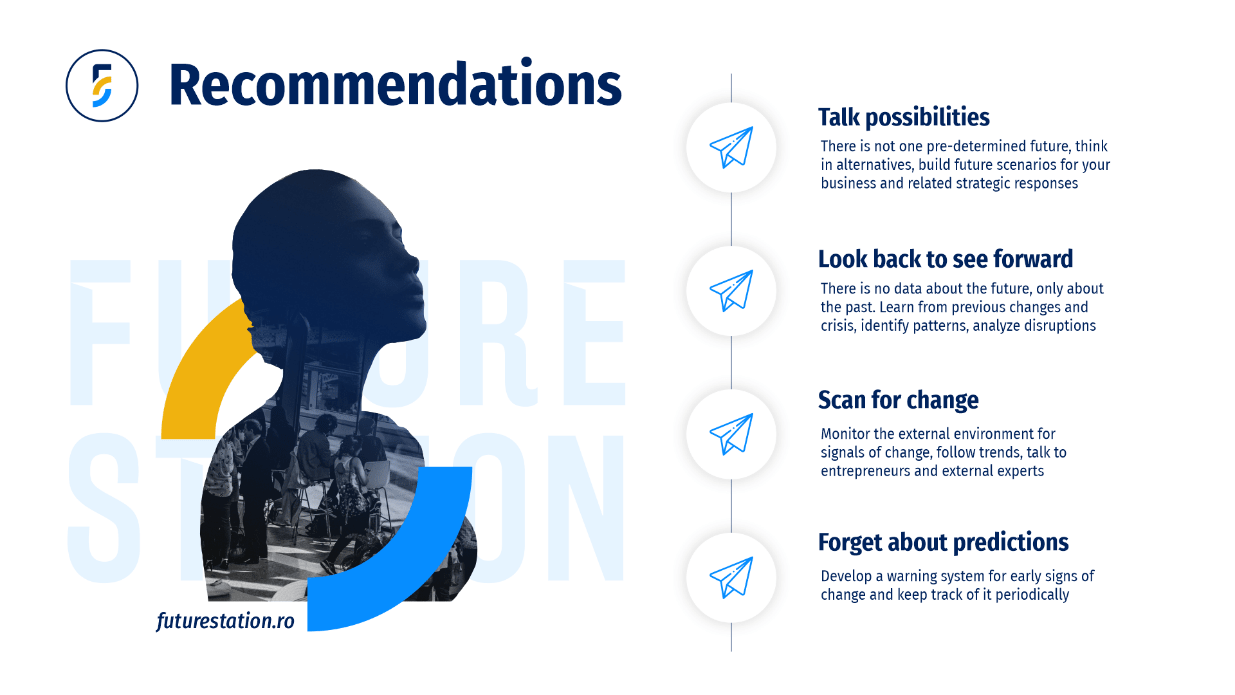

Recommendations

It’s time to face the facts, do not underestimate the uncertainty and prepare for the future:

- Talk possibilities

- Look back to see forward

- Scan for change

- Forget about predictions

Join the Conversation

We’d love to hear what you have to say.

Get in touch with us on our LinkedIn Group, Facebook Group or Twitter.

9 emerging consumer trends (2020-2021)

Saying the past year has been eventful is an understatement. With so much going on in the world right now, consumer behaviour was bound to change.

Here are 9 emerging trends in consumer behaviour for 2020-2021

1. Livestreaming + Shopping = Shopstreaming

Viya is China’s star saleswoman with a $60 billion ecosystem of live online shopping.

She is 34 years old and in May 2020, she hit a record-high audience of more than 37 million, more than the “Game of Thrones” finale or the Oscars.

Viya sells everything: from cosmetics to furniture to doorbells, but she also sold cars, houses and a rocket launch.

Her livestream show is a combination of several current tech trends—streaming, influencers, social, commerce and it’s a success many only dream about: each night her audience places orders worth millions of dollars.

Viya is not the first livestream sensation. In 2017, pearl businessman Xinda Zhan nicknamed Pearl Bro made $4.4 million in half a year from live-streaming the process of harvesting the pearls.

2. Growing our own vegetables

According to the latest statistics, 76% of the world’s population now live in urban areas.

People’s need for a closer supply of nutritious food has increased in recent years, and the pandemic enhanced it even further.

Urban farming or vertical farming is on the rise globally, and innovative technologies provide people turned urban farmers with tools to help them grow more produce at less space.

Urban farming is sustainable and clean: urban farmers grow their own vegetables in indoor spaces free of pesticides or herbicides. A 2019 study reports that global urban farming is expected to reach $288.71 billion by 2026.

Agricool founders: Guillaume and Gonzague / image source: agriculture.gov.fr

Agricool is a French startup growing vegetables and strawberries in shipping containers before selling the produce in stores within 15km of where the food was grown. The company has raised around $39m to date.

3. Seeing the doctor is now going digital

Today the world is still fighting the coronavirus pandemic with serious consequences for every one of us. At the time of writing, twenty-five million people have been infected and you can count the number of COVID-19-free countries on one hand.

Digitalization, albeit forced has been one of the positive changes (if not the only one) the pandemic has brought to the business environment.

Healthcare is one of the industries that require an in-person presence at a specific location: a doctor’s office.

With every country asking its citizens to go into quarantine and avoid public spaces as a measure to fight the pandemic, healthcare providers have adopted the digital solution: doctors consult, monitor and treat their patients online whenever the situation allows.

Vocalis Health is a tech startup which uses voice to monitor health. The company’s AI-driven software assists healthcare workers with screening and monitoring patients with a variety of voice-affecting diseases, including chronic respiratory or cardiac conditions or depression.

Tele-ICU is a centralized remote patient monitoring centre enabling off-site clinicians to interact with bedside staff to consult on patient care.

How does it work? Using A/V conferencing and a real-time data-stream of patient information from multiple interfaces, a physician working from a care centre in New York City can rapidly care for a patient in Seattle, day or night.

Other healthcare providers have set up virtual clinics where patients communicate with doctors via live video and audio. The patient saves on transportation time and costs.

According to GlobalWebindex, 70% of internet users in the U.S. and the UK believe technology will play a key role in managing their health and wellbeing in the near future. 50% of said the ability to find doctors and make appointments online, to access all of their health information online and consult with a doctor by a phone/video call could help them manage their health more effectively.

Also, the report found there’s strong demand for digital health technologies such as a symptom checkers, wearable devices to monitor health, health tracking apps, digital health assistants or digital health coaches.

4. Design a home that is good for you

Homo sapiens built out of necessity – to protect his family from nature’s elements and hungry predators. The early ancient civilizations – the Egyptians, the Chinese, the Mesopotamians built structures as a testament to their culture and civilization. Modern civilizations benefited from advanced technology. But this was not always good for our health.

In the 20th century, sick building syndrome was identified, a medical condition where people in a building suffer from symptoms of illness or feel unwell for no apparent reason. This syndrome is linked to various causes: inadequate ventilation, deteriorating fibreglass duct liners, chemical contaminants from indoor or outdoor sources, biological contaminants, traffic noise, poor lighting, moulds.

In the 1990s, new standards of construction were developed designed to protect the environment such as the BREEAM and LEED standards.

In recent years, a new standard has been implemented – the WELL Building Standard.

image: greenengineer.com

The WELL Building Standard is defined as “the premier standard for buildings, interior spaces and communities seeking to implement, validate and measure features that support and advance human health and wellness.”

The standard covers seven core design aspects: Air, Water, Light, Nourishment, Fitness, Comfort, and Mind.

5. The premiumization of human contact

Technology pervades almost every aspect of our daily lives. The smartphone that we all have in our pockets serves many of our needs from communication, placing orders for food, clothes, transportation to booking appointments with our doctor or coach and taking exams or being entertained.

In the past few years, voice assistants have become very popular whether integrated into our smartphones or standalone such as Amazon’s Alexa. They have influenced consumer behaviour (voice shopping) which has given rise to a new type of commerce – voice commerce.

62% of those who regularly use a voice-activated speaker say they are likely to buy something through their voice-activated speaker in the next month and 44% say they order products (groceries, household items, etc.), at least once a week (discover more about how voice is changing customer behaviour).

Yes, technology is convenient and helps us do things faster, but technology is not a proxy for the human connection.

And having human interaction is something we long for and ultimately need to maintain balanced mental health.

In 2019, 62% of global internet users said they are constantly connected online. What does that mean in hours a day? Almost 7 hours online every day compared with 5 hours and 36 minutes in 2012. And that’s not good for our health, sleep, and relationships as we have become increasingly prone to anxiety and depression.

Everyone has access to technology: low-income and high-income alike.

Unplugging from technology is another thing and as the GlobalWebIndex report shows, the affluent have the freedom and power to unplug. Going technology-free is expensive and only the rich can afford it.

High-income levels are also associated with a preference for human-driven customer service.

52% of high-income earners said they typically interact with a business face-to-face compared with 42% of low and 41% of middle-income earners.

When asked what their preferred method of interaction is, high-income earners were nearly twice as likely as middle and low-income earners to say that it’s face-to-face interaction with a human.

Brands offer human-driven customer service as a premium service: talking to a chatbot costs less than talking to a human representative.

6. Digital OOH for consumers in motion goes underground

With high-income earners unplugging from digital screens and 48% of internet users employing an ad blocker, how are brands going to reach their consumers?

Out-of-home advertising or OOH may be one of the available solutions for marketers.

According to GlobalWebIndex stats, OOH focused on consumers in motion is poised to hit the next level of mass reach, visual impact and location targeting in 2020.

Thanks to developments in OOH technology, brands can serve consumers dynamic creatives based on environmental factors such as weather, location and time of day.

This makes advertisements highly-relevant and when combined with a little bit of entertainment, it could influence consumer’s behaviour.

In the UK, video OOH now reaches more than 32.5 million people each month—that’s nearly half the population of the UK, and a broadcast reach that historically only TV has been able to offer.

56% of those in the U.S. and UK who travel by an underground or subway system said they could recall a billboard ad from the last week – markedly higher than the number of train (44%) and bus travellers (47%) who said the same.

35% of travellers by underground said they searched for something and later made a purchase after seeing a billboard ad in the last week.

Do you plan to use DOOH?

Go underground for maximum results!

7. Car, order three chicken wings, a pound of cheese and one milk bottle! – The commuting consumer

As you’ve read in this article, voice assistants live in our homes and are an integral part of smartphones.

But what about our cars?

The average American spends 10 hours and 50 minutes in their cars per week. While driving, there isn’t much you can do except listening to music or immerse yourself in thoughts. If you would like to order something for dinner, you could do so by using your car’s embedded voice assistant.

BMW Intelligent Personal Assistant/source: press.bmwgroup.com

Connected cars embedded with voice assistants are growing in number.

BMW has already integrated Amazon’s Alexa into their cars and Visa provides its partners with Visa Token Service, an in-car digital wallet which makes payments simple and secure.

8. ‘Cancel culture’ or ‘call-out culture’

According to the latest report of market intelligence agency Mintel, brands should expect to see a rise in consumer backlash over the next 10 years as consumers continue to find their voice in the digital era.

It’s a trend in consumer behaviour that has become increasingly visible following the latest changes in society calling for diversity in the business world. The Mintel researchers call it the ‘cancel culture’ or ‘call-out-culture’.

Consumers want companies and brands to stand for something.

Think Nike’s Dream Crazy, Iceland’s banned TV Christmas Advert Say Hello to Rang-tan, Gillette’s The Best Men Can Be or Barbie’s Close The Dream Gap (read about them).

While some are controversial, every one of these ads raised awareness on a specific subject that brands haven’t tackled yet.

When brands fail to do the right thing by their employees, they are met with protests and call-outs.

2018 Google walkout/image source: nytimes.com

In 2018, 20,000 Google employees walked off the job in protest of the company’s handling of sexual harassment allegations, turning tech workers into activists.

For some brands, change is now coming from employees putting pressure on the management, not the other way around. Brands are urged into updating their rules and regulations to provide every employee with equality and transparency.

With Black Lives Movement extending worldwide, consumers are expecting workplaces to become more diverse and inclusive. Some brands have been called out for joining the movement just to tick another box or for being disingenuous.

9. Consumers as owners of their data

In exchange for convenience and personalized experience, brands told consumers to give their personal data and relinquish any control over it.

We now know how brands used their consumers’ data and the damage they have caused.

According to the latest PwC report, consumers are demanding both a better, data-enabled experience and more flexibility and control over how their information is used.

New regulations around data privacy and security support consumers acting like owners of their data and slowly recognising that it has commercial value.

Californian businesses are required to provide “a good-faith method for calculating the value of the consumer’s data.”

Respondents said they were willing to share their personal information under certain conditions which included the following:

– receiving financial compensation for it,

– enjoying a more personalised experience,

– being able to share data with only those they trust or not sharing it with third parties under any conditions.

Conclusion

There you are – 9 emerging trends in consumer behaviour.

How is your brand going to capitalize on them?

Are any of them relevant to your industry?

Join the Conversation

We’d love to hear what you have to say.

Get in touch with us on our LinkedIn Group, Facebook Group or Twitter.