Return On Experience (ROX) Is The New Return On Investment (ROI)

You may be familiar with Return on Investment as a metric but do you feel you need an additional performance measurement tool which illustrates more accurately the changes in our world with a direct impact on your business?

PwC offers you the answer to your question – Return on Experience.

What is ROI?

Return on Investment (ROI) is a performance measure used to evaluate the efficiency of an investment. To calculate ROI, the benefit (or return) of an investment is divided by the cost of the investment. The result is expressed as a percentage or a ratio.

ROI is a financial metric of profitability widely used in business. With the rise of digital and social media, business executives may find it difficult to calculate the ROI of their company’s marketing and advertising efforts on digital platforms.

What’s the ROI of social media?

Some digital experts believe that due to its human nature social media cannot be measured using a business-focused tool. Three years ago Gary Vaynerchuk famously replied to a business executive asking him repeatedly about the ROI of social media with What’s the ROI of your mother?

Other digital experts support the idea of looking at social media from a different standpoint – that of soft leads generator which I believe is more accurate. Marketers should find where social media fits best in their company’s funnels so that their efforts translate into results that can be measured.

Consumers have power over brands

Our world is changing; it’s not technology leading the change, it’s the people. It’s not the businesses running the show, it’s their consumers. They have power over brands, not the other way around.

According to PwC’s 2019 Global Consumer Insights Survey, it’s time to include another metric in addition to the traditional ROI. It’s the consumer-centred metric – the Return On Experience or ROX.

We need to introduce another metric, one with a laser focus on customer experience: return on experience. Whether your organisation is in the business of household goods, health services, selling cars or financial services, delivering a superior experience will be what makes you a winner.

PwC – 2019 Global Consumer Insights Survey

What is ROX?

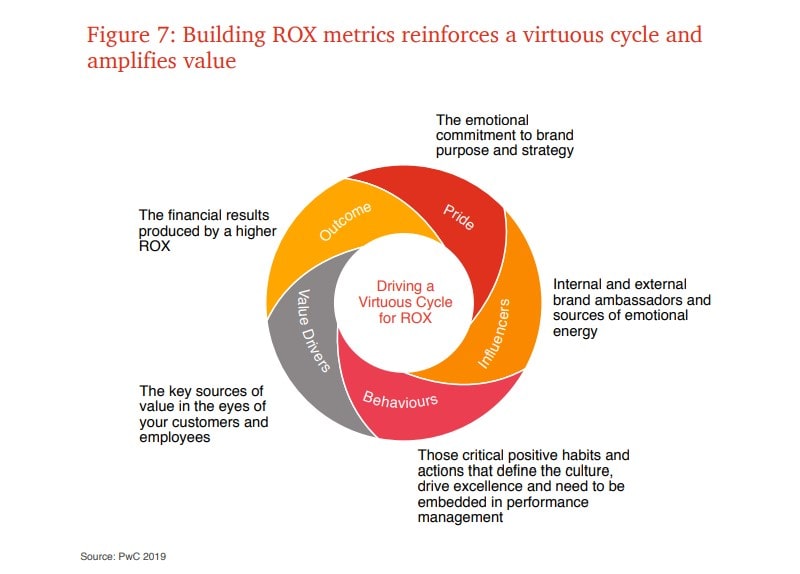

The Return On Experience (ROX) is the metric with which marketers measure the purchase experience of their consumers.

Because consumers today are so discerning and powerful, it’s our perspective that most organisations need to invest far more in customer experience (CX). Measuring ‘return on experience’ (ROX), will help you understand your earnings on investments in the parts of your company directly related to how people interact with your brand.

John Maxwell, PwC’s Global Consumer Markets leader

Why should you include ROX in your measurement list?

Here are 10 of the report’s main findings which are good reasons for your company to include ROX as an additional measurement metric:

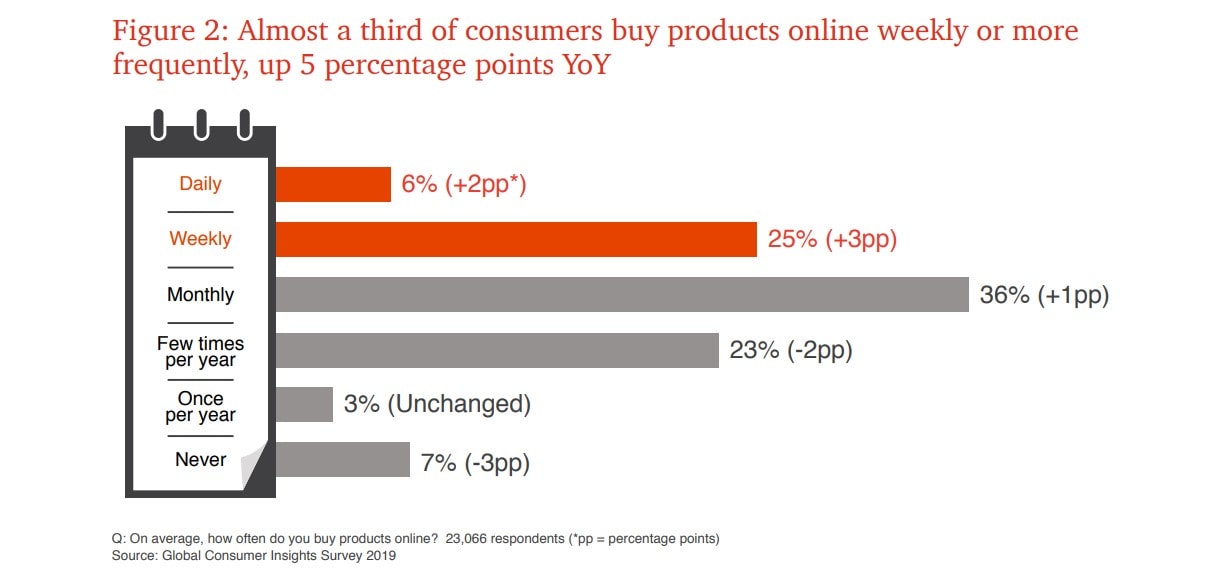

- 31% of consumers buy online weekly or daily;

- 24% of consumers shop on smartphones more often than on PCs – the first year in the decade PwC has been conducting this study that mobile phones were used more than other digital devices;

- 51% of respondents paid bills and invoices online;

- 51% transferred money online;

- 54% are streaming movies and TV 2x a week or more;

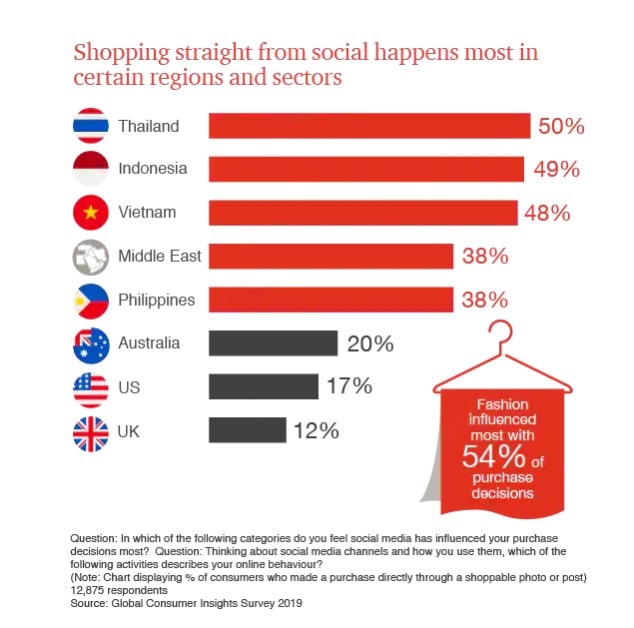

- 39% of Gen Z respondents said they go directly to social media for information compared with 25% overall;

- Mobile payment has been growing steadily since 2018, with China leading the way (86%) followed by Thailand (67%), Hong Kong (64%) and Vietnam (61%);

- 75% of consumers are using their mobile phones for health information;

- 46% of consumers would like to have an autonomous vehicle today or would consider one in the future;

- 35% of the survey’s respondents said they choose sustainable products to help protect the environment, 37% look for products with environmentally friendly packaging, and 41% avoid the use of plastic when they can.

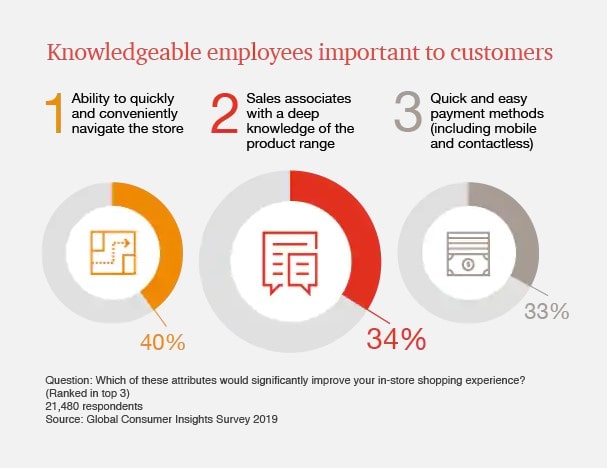

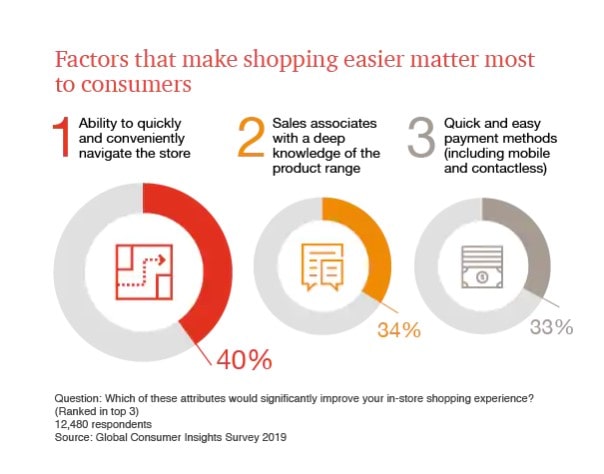

Now that you’re convinced of the power of your consumers and the importance of the customer experience, let’s see what factors contribute to great customer experience.

5 factors who drive great customer experience:

1. Less friction

Your company should aim towards a frictionless purchase journey. A purchase journey which eliminates friction as much as possible encourages your customers to buy more frequently and spend more money.

Amazon is a great example of a frictionless purchase journey.

2. Digital voice assistants

9% of consumers said they used voice technology to shop online weekly or more frequently. Using digital voice assistants makes it easier for consumers to buy. The voice technology contributes to the frictionless purchase experience.

Learn more: What Voice Search and AI Mean For Your Business

3. BOPUS

BOPUS is the acronym for buy online and pick up in store. BOPUS requires previous customer training but it works because it is convenient.

4. Blended experiences

A blended purchase experience means augmenting your customer’s in-person interaction with digital content before, during and after that interaction.

5. Employee experience (EX)

Last but not least, the employee experience is vital to creating excellent customer experiences. It means your company should invest in and improve the employee experience (EX) because EX has a big impact on customer experiences.

Learn more: Keeping Your Employees Happy Is More Than A Higher Paycheck

Are you looking to improve your ROX?

Based on the PwC survey results, here are 6 recommendations on how your company can improve its Return on Experience:

1. Fuse CX and EX

Companies that invest in and deliver superior experiences to both consumers and employees are able to charge a premium of as much as 16% for their products and services.

2. Build communities with a purpose;

3. Build on discreet moments along the customer journey;

4. Understand your customers based on their behaviours;

5. Treat consumers’ data with respect, and deliver value in exchange for it;

6. Win the trip.

Win over customers on-premise or via e-commerce by understanding what they are trying to experience and then making it easier for them to accomplish that goal.

Design your ROX-focused framework

What should your ROX-focused framework look like?

- Identify the things your company does exceptionally well;

- Make sure your IT systems, data infrastructure, business processes and performance metrics are aligned with those core capabilities;

- Identify your company’s ‘critical few’ behaviours; these behaviours are the ones that are most important to creating and delivering excellent customer and employee experiences;

- Quantify your progress in building these behaviours across functions, business units and geographies;

- Use your metrics to gain deeper insights into what matters most to customers;

- Quantify what’s most important along the path to purchase and what factors are most influential in driving customer behaviours.

Join the Conversation

We’d love to hear what you have to say.

Get in touch with us on Facebook Group and Twitter.

PwC: 5 MegaTrends Affecting Your Business in 2019 (2 of 2)

PwC has identified 5 global Megatrends that shape our world. This article explores these Megatrends looking at the way they affect the global business environment.

As business owners and entrepreneurs it’s paramount to have a good grip on the present and also stand on the threshold of the future.

Let’s see how these Megatrends identified by PwC are shaping our business environment on a global scale and what you can do to make the best of them.

This article is delivered in two parts. Read the first part:

PwC: 5 MegaTrends Affecting Your Business in 2019 (1 of 2)

4. DEMOGRAPHIC AND SOCIAL CHANGE

By 2030 the world’s population is projected to rise by more than 1 billion. Equally significantly, people are living longer and having fewer children.

PwC

Challenges

By 2030 the world’s population is projected to rise by more than 1 billion, bringing the total to over 8 billion.

Emerging or developing countries will produce 97% of this population growth.

People are living longer and having fewer children.

People over 65 is the fastest growing segment of population – according to PwC there will be 390 million more of them in 2030 than in 2015.

Many advanced countries are seeing their population working age slow down its growth.

Inequality is a rapidly rising trend. To illustrate this, PwC gives the following example:

The world’s 8 richest people now own as much wealth as the poorest half of the world’s population.

The shift in demographic profile will bring disruption to the traditional life cycle of education, work and employment.

The ageing population has a direct influence on healthcare spending – it will increase. But an ageing population also means an untapped resource and businesses need to find ways to take advantage of this opportunity.

[bctt tweet=”People over 65 is the fastest growing segment of population” username=”brand_minds via @PwC_UK”]

Solutions

Here’s how businesses can take advantage of the demographic shift:

- Businesses must find ways to stimulate, incentivize and empower young people;

- They also need to harness the power of older workers and women.

There are various measures that businesses can adopt to encourage older workers to remain in the workforce:

- Create more flexibility around retirement;

- Create financial incentives;

- Adopt reforming pension rules;

- Outlaw age discrimination;

- Re-training;

- Reverse mentoring;

- Phased retirement;

- Training and apprenticeships that are normally addressed to younger recruits.

BMW is one of the companies which is leveraging the power of ageism: they have redesigned their factories for older workers.

Sweden is the best performing EU country in regard to older workers employment rates. According to PwC,

The G7’s GDP could increase by as much as $1.8 trillion in the long-term; if the G7 economies could achieve the same level of full-time equivalent employment rates among the over 55s as Sweden.

Women are a great resource for the workforce, but businesses are yet to leverage it at its full capacity.

- Women become mothers later in life and have fewer children;

- Women are a growing purchasing power: according to PwC 70% of household budgets in the G7 are controlled by women, globally 85% of consumer purchases are made by women which is equivalent to a worldwide spend of $20 trillion;

- Hiring women is highly beneficial to businesses worldwide. Reports have shown that companies with a higher percent of women in high management roles are constantly outperforming those with fewer women.

Peterson Institute for International Economics found that firms with more women in the C-Suite are 15% more profitable.

PwC

Women represent an invaluable pool of talent, skills and abilities and to attract and retain them, businesses need to take the following steps:

- Ensure that all employees are receiving fair pay and promotion;

- Support women’s career advancement to develop a pipeline of female leaders;

- Promote flexible working options.

Learn more about global recruiting trends: Global Recruiting Trends 2019 – LinkedIn Study

[bctt tweet=”Women are a great resource for the workforce, but businesses are yet to leverage it at its full capacity.” username=”brand_minds via @PwC_UK”]

5. TECHNOLOGICAL BREAKTHROUGHS

By 2020 there will be close to seven times the number of connected devices as people on the planet.

The digital revolution has no boundaries or borders. It is changing behaviour and expectations as much as the tools used to deliver new services and experiences.

PwC

Challenges

PwC has found that emerging economies are adopting technologies as fast – or in some cases faster – than developed markets.

Due to the digital revolution, the scale of the business is no longer an insurance regarding its competitive advantage, as we have shown in our Failure Series articles regarding Nokia and Kodak.

For many years, corporate technology was far more advanced that anything available to the consumer. But two key dates – 2007 and 2010 (the launches of the iPhone and the iPad respectively) – decisively shifted this imbalance in favour of the consumer.

PwC

The digital revolution has ushered in a shift in power from corporate to consumer. Now it’s the consumers driving the specifications of corporate technology, not the other way around.

The digital way of life is personified by the Millennials, the generation who was not required to adapt to digital because they were born into it. For them, technology is a form of natural language. To include the Millennials into workforce, businesses must direct their activities to fit this aspect.

Together with digital comes another important trend: social media.

Organisations need to understand that social media is not simply another channel, but a fundamentally new and different way in which people organise and live their lives. And its scale, already vast, is growing constantly.

PwC have identified the following maturing technologies:

- AI;

- Augmented Reality;

- Virtual Reality;

- IoT;

- Blockchain;

- Drones;

- Robots;

- 3D printing.

They believe these technologies offer huge potential in many industries. Their word of warning to businesses looking to embrace them is as follows:

Don’t adopt these technologies for their own sake. Experiment and learn from these technologies with the clear purpose of finding how to use them to create value. If implemented correctly, businesses can benefit galore in way of producing financial wealth.

Connected homes, connected cars, virtual interfaces, smart locks etc. – everything is connected. While ubiquitous connectivity has numerous advantages, it is not risk free. The upside of all things connected is that it is a gateway to consumer behaviour data which was previously untapped.

Many of today’s largest and leading organisations and businesses were developed in an era of scarce, expensive and rigid technology. Delivering change for them is a complex proposition. On the contrary, businesses that are ‘born digital’ are much better prepared to deal with the constant flux of change that hits everyone.

[bctt tweet=”The upside of all things connected is that it is a gateway to consumer behaviour data which was previously untapped.” username=”brand_minds via @PwC_UK”]

Solutions

MIT Sloan School of Management has found that large organisations run a greater risk of disappearing due to digital disruption over the next 5 years. The solution is the emergence of four distinct types of business model:

- Omni-Channel;

- Supplier;

- Ecosystem Driver;

- Modular Producer.

Join the Conversation

Get in touch with us on Facebook and Twitter. We’d love to hear your views!

source: https://www.pwc.co.uk/issues/megatrends.html

PwC: 5 MegaTrends Affecting Your Business in 2019 (1 of 2)

PwC has identified 5 global Megatrends that shape our world. This article explores these Megatrends looking at the way they affect the global business environment.

As business owners and entrepreneurs it’s paramount to have a good grip on the present and also stand on the threshold of the future.

Let’s see how these Megatrends identified by PwC are shaping our business environment on a global scale and what you can do to make the best of them.

Megatrends: 5 global shifts affecting your business in 2019

- Rapid urbanisation;

- Climate change and resource scarcity;

- Shift in global economic power;

- Demographic and social change;

- Technological breakthroughs.

1. RAPID URBANISATION

Today, more than half the world’s population live in urban areas and almost all of the new growth will take place in lesser known medium-sized cities of developing countries.

PwC

Challenges

Increasing global urban population: 1.5 million people migrate to cities every week.

Cities generate most of the world’s GDP: 85% in 2015.

Cities stay at the heart of any economic development because they harness the power of economies of scale; they add value for people and companies thanks to their ability to attract talent, ideas, share knowledge and support businesses development.

Cities elevate the living standards of their citizens. China is an excellent case in point:

500 million Chinese people were lifted out of poverty in less than 30 years becoming China’s booming middle class thanks to their developing cities.

[bctt tweet=”Cities represent a major opportunity for business thus becoming breeding grounds for wealth-creation” username=”brand_minds via @PwC_UK”]

To achieve that, cities must do the following:

- Increase competition with other cities for talent, investment and firms;

- Enhance levels of participation in city governance;

- Improve connectivity;

- Stimulate small business enterprises;

- Deliver inclusive infrastructure;

- Support sharing economies and micro industries.

One of the major opportunities that comes for the business environment is the emergence of new business models for delivering public services.

The current model of urbanisation is unsustainable. A crucial policy implication for government and business is not just to make the mega city workable but to address the urbanisation challenge at its source by helping to combat the distressed migration of 200,000 people a day from the countryside to the city.

PwC

The direction in which cities develop and evolve is shaped by the joint actions of city governments, citizens and businesses.

Solutions

- Businesses must act towards taking greater responsibility for the following: service delivery, infrastructure investment, environment protection etc;

- Job creation.

source: PwC

For large international businesses, rapid urbanisation will mean the creation of new markets. In their effort to expand globally, these companies should adopt a careful approach on how to position themselves in order to tap into the newly discovered potential.

Businesses will also see a change in their behaviours too.

The private sector will be challenged to be more open, sustainable, collaborative, innovative and flexible in their approaches.

PwC

2. CLIMATE CHANGE AND RESOURCE SCARCITY

As the world becomes more populous, urbanised and prosperous, demand for energy, food and water will rise. But the Earth has a finite amount of natural resources to satisfy this demand.

PwC

The world’s current economic model is pushing beyond the limits of the planet’s ability to cope.

Challenges

In the last years, the scientific community’s predictions were proven to be right. Unfortunately they were accurate about the rate and effect of human impact on the climate.

The planet is no longer able to support current models of production and consumption.

The rising temperatures are predicted to lead to significant and potentially irreversible environmental changes. The pressure on natural resources is expected to increase dramatically.

The numbers show that a growing global population will also mean a 35% increase in food demand by 2030. Also demand for water will increase by 40% and for energy by 50%. In Africa, another consequence of climate change is reduced agricultural productivity by ⅓ over the next 60 years.

The link between trends in climate change and resource scarcity is a stark reality and needs to be addressed appropriately.

Solutions

The global economic development will be sustainable, or it won’t be at all.

Businesses that are largely dependent on natural resources – water, land, energy – or are polluting the environment have already begun their transformation journey into responsible, ethical, waste-reducing companies. In order to achieve this goal, businesses have embraced innovation.

Learn more: Dell and Nikki Reed – Gold Jewellery made from Electronic Waste

Unpredictable climate changes and environmental policies will bring organisational changes. Businesses must assume a leading role in alleviating environmental damage while working internally to adapt to changes by adopting organisational agility.

Learn more: 22 Benefits of the Agile Organisation

Businesses must reassess their purposes. In order to survive in this challenging environment, businesses must acknowledge the need to become more than a source of profit for their shareholders. Business leaders need to look further and beyond earning money; they need to understand and measure their company’s impacts on society and environment. Businesses need to develop an ecosystem that spans over a longer period of time for ROI.

[bctt tweet=”The global economic development will be sustainable, or it won’t be at all.” username=”brand_minds via @PwC_UK”]

Companies need to become aware that moving towards a business model that is sustainable and ethical is a powerful differentiator. As various reports show, 66% of global Millennials are willing to spend more on brands that are sustainable.

3. SHIFT IN GLOBAL ECONOMIC POWER

Challenges

Between 2014-2016 many emerging markets experienced a decline in economic performance when commodity prices dropped.

Here are a few examples:

- Brazil and Russia are now in recession;

- A former champion of economic growth, China is slowing down;

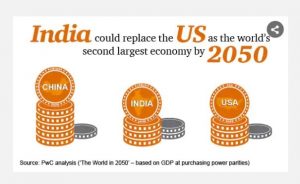

- On the other hand, India is growing thanks to the following: being a net importer of oil and other commodities and therefore a beneficiary of lower global prices, more business-friendly policies to stimulate economic development and growth.

PwC has projected that

India could overtake the USA as the world’s second largest economy by 2050 (based on GDP at purchasing power parities) and should be the third largest economy ahead of Japan by 2030.

source: PwC

Solutions

Businesses that are investing, or already invested, in emerging economies will need to make a careful assessment of whether and, if so, how they should manage in these more volatile market conditions, where prospects look less certain today than they did even a few years ago.

[bctt tweet=”Brazil and Russia are in recession, China is slowing down, India is growing. ” username=”brand_minds via @PwC_UK”]

Join us next week to read part 2 of PwC: MegaTrends Affecting your Business in 2019.

Join the Conversation

Get in touch with us on Facebook and Twitter. We’d love to hear your views!

source: https://www.pwc.co.uk/issues/megatrends.html