Global Recruiting Trends 2018 – LinkedIn Study

LinkedIn is the main social platform for recruiting purposes.

Latest statistics show there are more than 562 million users on LinkedIn in over 200 countries, more than 15 million jobs are listed on LinkedIn Jobs and professionals are signing up to join LinkedIn at a rate of more than two new members per second.

The collected data and info allowed LinkedIn to research global recruiting trends for 2018.

Find out the 2018 global recruiting trends, discover how various companies apply them to their hiring processes and see the results these new tools have brought them.

[bctt tweet=”Global Recruiting Trends 2018 – LinkedIn Study @LinkedIn” username=”brand_minds”]

Global Recruiting Trends 2018 – LinkedIn Study

In the latest years, the hiring process has become highly inefficient. Tedious candidate searches, endless scheduling and repetitive screening have made it hard for recruiting professionals to find and attract valuable candidates. But there is hope on the horizon for both companies and candidates!

The LinkedIn study revealed 4 recruiting trends:

- Diversity;

- New interviewing tools;

- Data;

- Artificial Intelligence.

Companies interviewed by LinkedIn have found these tools to directly impact their recruitment process.

If you wish to increase the quality of your candidates and to improve your hiring process, keep reading!

1. DIVERSITY

Diversity used to be a box that companies checked. But today, diversity is directly tied to company culture and financial performance. LinkedIn data shows that 78% of companies prioritize diversity to improve culture and 62% do so to boost financial performance.

Companies that didn’t adapt to changing demographics have realised their talent pools were shrinking. Evidence has showed the benefits of diverse teams: increased levels of productivity, innovation and engagement.

Top reasons companies focus on diversity:

- 78% to improve culture

- 62% to improve company performance

- 49% to better represent customers.

Many companies fall short on achieving their diversity goals because they are not looking in the right places.

Diversity Challenges

Here are the biggest challenges that companies face when looking to improve diversity within the company:

- 38% cannot find diverse candidates to interview;

- 27% fail to retain diverse employees;

- 14% fail to get diverse candidates past interview stage;

- 8% fail to get diverse candidates to accept offer.

How do companies show candidates that they value diversity?

- 52% use diverse employees in web and print materials;

- 30% talk about ERGs;

- 35% present diverse interview panels;

- 28% recruit at schools with diverse student bodies.

Dos and donts:

- Do use inclusive language in your job descriptions

Inclusive language will broaden the appeal of your opportunities and let you reach more diverse talent.

- Do empower employees to tell their stories

The storytelling exercise itself will boost engagement with employees while growing your reach with diverse candidates in an authentic way.

- Do promote inclusion and advocate change with ERGs

You have much more diversity power when you can lean on the natural momentum of grassroots groups.

- Don’t have a diversity “strategy.”

Think of it as a mindset instead. Start small to effect change. Weave it into everything your company does, little by little.

- Don’t invest without buy-in from the top

You won’t go far if your leaders aren’t sold on the value of diversity. The bottom line will always grab their attention so make your case with numbers.

- Don’t perpetuate the appeal of “culture fit”

Change the bar with which you assess talent from “culture fit” to “culture add” to better create a culture of differences.

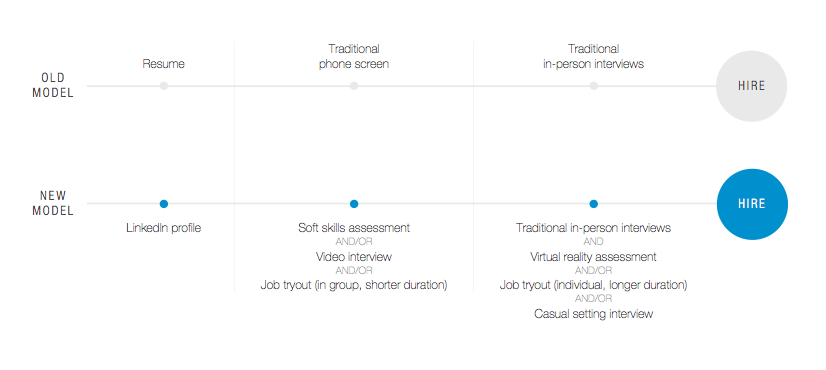

2. NEW INTERVIEWING TOOLS

Interviewing is the most widely used tool by recruiters. That being the case, traditional interviews have many flaws and hiring experts have detailed where they fall short.

Interviewing Challenges

- Assessing candidate soft skills – 63%;

- Understanding candidate weaknesses – 57%;

- Bias of interviewers – 42%;

- Too long of a process – 36%;

- Not knowing best questions to ask – 18%.

To get different results, recruiters have changed the way they conducted the interviews.

Interviewing Innovations

Here is how recruiters improved their interviewing strategies:

- 59% used soft skills assessments;

- 54% conducted job auditions;

- 53% met with candidates in casual settings;

- 28% conducted virtual reality assessments;

- 18% interviewed candidates through video.

“Take a look inside their heart, rather than their head.”

Walt Bettinger

CEO of Charles Schwab

Companies using new interviewing tools:

- Citi piloted the Koru7TM, a 20-minute survey that ranks candidates’ soft skills strengths and weaknesses which allows Citi to conduct more informed interviews;

- Jet.com interviewed candidates on ferris wheels;

- Daimler AG took candidates for a spin in a Mercedes;

- Lloyds Banking Group evaluated candidates in virtual reality as part of a day-long assessment center visit;

- KPMG used video interviews to evaluate candidates’ skills at scale, before even meeting them.

LinkedIn Global Recruiting Trends 2018

LinkedIn Global Recruiting Trends 2018

“We were hiring based on experience and not potential, and the profile of our leaders yesterday will not be the same profile for our future leaders. Our process was not fit for purpose in the connected world.”

Melissa Gee Kee

Strategy Director to the CHRO, UNILEVER

Benefits and results of new interviewing tools:

- Better assessment of soft skills;

- More talent pool diversity;

- Positive candidate experience;

- Better ability to see character;

- Candidates can try out job for fit – 59%;

- Less bias than traditional formats – 47%;

- Video has cut the number of in-person interviews from thousands to hundreds, freeing up significant recruiter time;

- The hiring process changed from experience based to potential based;

- More realistic snapshot of candidate’s personality – 69%;

- Candidates can’t lie about skills – 26%.

3. DATA

Most recruiters and hiring managers use data in their work now and even more are likely to use it in the next two years.

Data can be used to predict hiring outcomes, not just track them. Data can power machines to make smarter recruiting decisions for recruiting experts.

How companies use data in talent acquisition:

- 56% to increase retention;

- 50% to evaluate skills gaps;

- 50% to build better offers;

- 46% to understand candidate wants;

- 41% to do workforce planning;

- 39% to predict candidate success;

- 38% to assess talent supply and demand;

- 31% to compare talent metrics to competitors’;

- 29% to forecast hiring demands.

Data-based recruiting challenges

What prevents hiring managers to use data?

- 42% say the quality of collected data is poor

- 20% are not sure where to get it

- 18% say data is too expensive

- 14% are not sure how to use it.

Companies using data-based recruitment:

- Nielsen used data to find out what was the reason for losing talent and how to prevent it: thanks to collected and analysed data, they found that employees with a change in job responsibilities due to promotion or lateral movement within the past two years were much less likely to leave;

- Novartis leveraged data from LinkedIn to decide where to open its new office;

- With the help of its customer feedback data, JetBlue tweaked its target profile;

- Atlassian used internal data and LinkedIn’s talent pool reports to pinpoint key European markets where the supply of tech talent exceeded the demand.

“Data is the one language that everybody speaks across the company. I gain trust from people across functions by bringing something that can be verified, something that can be checked.”

Bret Larson

Director, Talent Management & Analytics, EMERSON

Benefits and results of data-based recruiting:

- Increased employee retention thanks to more opportunities being offered to them;

- Faster decision making;

- Access to passive talent;

- Stronger employee engagement;

- Higher customer satisfaction;

- More international hires;

- Stronger employer brand;

- More credibility for talent acquisition professionals.

LinkedIn Global Recruiting Trends 2018

LinkedIn Global Recruiting Trends 2018

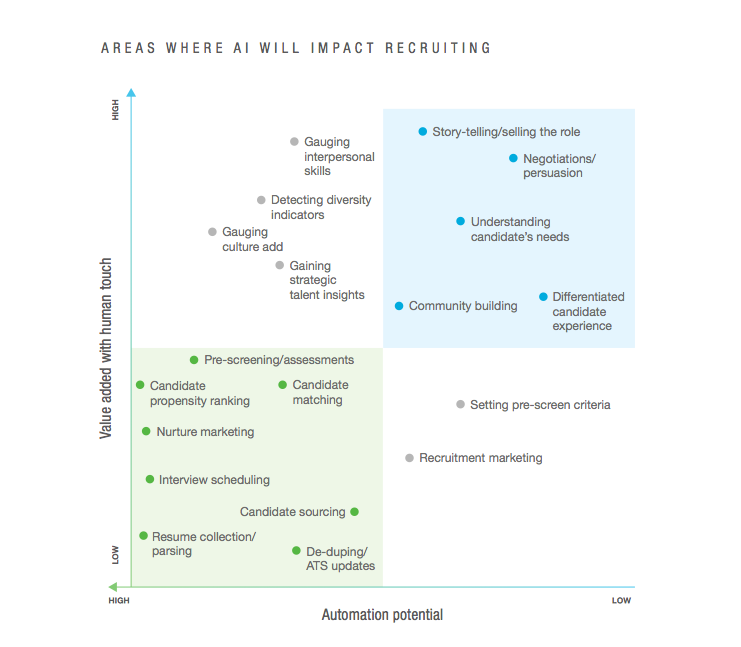

4. ARTIFICIAL INTELLIGENCE

This next-generation technology helps recruiters work faster by automating administrative tasks, and smarter by generating insights they wouldn’t think of alone.

Challenges of AI recruiting

Many recruiting professionals fear AI is going to take their jobs. But this assumption is not accurate.

AI doesn’t replace hiring professionals, it empowers them.

AI augments their jobs by analysing more information faster and smarter than they could ever do alone. It automates low-level tasks so they can focus more time on recruiting strategy and candidate relationships. LinkedIn’s research showed AI was least likely to replace the parts of the job that require personal and emotional engagement.

“Companies still need people — people to persuade and negotiate, to understand candidate needs, and to build communities and cultures. Paradoxically the more you use the technology, the more you can invest in the human side of the job.”

Artificial Intelligence supports companies as follows:

- 58% to source candidates;

- 56% to screen candidates;

- 55% to nurture candidates;

- 42% to schedule candidates;

- 24% to engage candidates;

- 6% to interview candidates.

LinkedIn Global Recruiting Trends 2018

LinkedIn Global Recruiting Trends 2018

Companies using Artificial Intelligence in their recruiting process:

- Intuit developed an algorithm-driven digital platform that scores and prioritizes candidates based on the profiles of its top performers;

- Vodafone used AI-powered software to screen its videos: based on role requirements, other candidates, and top performers at Vodafone, the machines assess candidate suitability;

- Deutsche Telekom AG used a chatbot to answer questions that potential applicants have about posted job offers: filtering out candidates who were not relevant (based on chosen criteria) and telling those poor-fit candidates that their chances of getting hired were low so applying wouldn’t be recommended.

“Recruiting can and should include tech—without making myself redundant. It lets me go back to being human as an HR person again.”

Anna Ott,

HR Expert, HUB:RAUM

Benefits and results of AI-based recruiting:

- 67% saves time;

- Bigger talent pool;

- 31% delivers best candidate matches;

- Better ability to assess soft skills;

- 43% removes human bias;

- Better candidate experience

- 30% saves money;

- Higher recruiter efficiency.

How Can Location Data Help You Grow Your Business

The importance of data is growing daily and its impact on the businesses as well. Gathered and used in smart ways it can help you reach the right audience, in the right way. In other words, it’s a known fact that location intelligence has become a fundamental part of some of the most successful businesses in the world today. Tough economic times and the advancement of new technology in recent years have massively pushed the need for businesses to gain more transparent and competitive insights on their performance and opportunities.

According to geovation.uk, location provides meaningful context. It can identify essential relationships between geography and consumer experiences, products and services. Location intelligence answers important questions, such as ‘where are my most valuable customers?’, ‘where are the issues impacting my supply chain?’ Location intelligence can detect clusters and patterns of events, make predictions, and provide the basis on which to make better business decisions.

Knowing the location of users, employees and company assets is becoming a vital part of many businesses in order to act efficiently and make informed decisions. From helping customers locate relevant amenities (e.g. Foursquare, Tripadvisor) to logistics companies optimizing delivery routes (UPS, Hermes), location, spatial data and digital mapping are playing a pivotal role in these business functions.

At the same time, location represents a great manner of revealing relationships between data sets that might not have otherwise been obvious and, through location analytics, arrive at great insights.

Worries about concerns like user privacy and data quality are valid: Know that it’s important to source location-informed insights from opt-in data that is thoroughly cleansed and, most importantly, aggregated and anonymized (the Location Search Association recently published a valuable landscape report analyzing the key providers in the space). Be sure to work with a data provider that adheres to emerging industry best practices, including use of data sourced only from apps with specific user opt-in (like Apple is now mandating), and complies with country-specific regulations, like GDPR. – entrepreneur.com

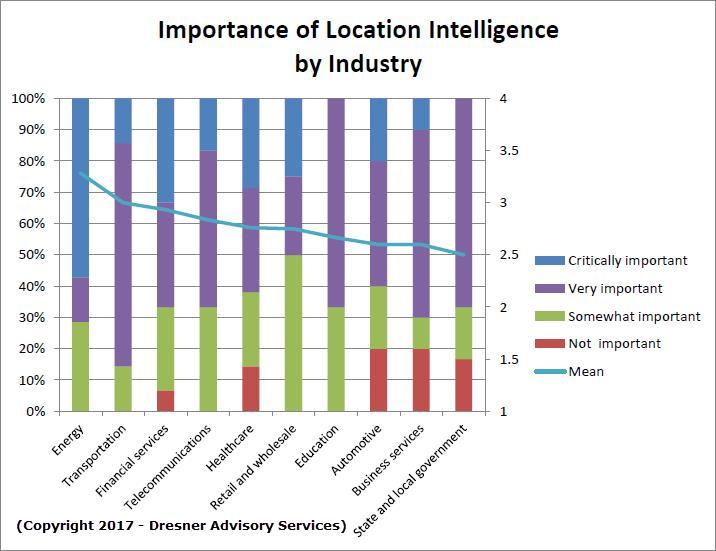

Data company Carto partnered with market research firm Hanover Research on a February 2018 study called “The State of Location Intelligence 2018,” surveying more than 200 C-level executives about the ways their companies are using location data to identify new consumer markets, improve marketing strategies and improve customer service. Here are some of their main findings:

- 66% of respondents said that Location Intelligence was “Very” or “Extremely” important today for their businesses, 78% said it would be in the next year, and 85% said it would be in the next three years.

- Only 27% said that they use any kind of custom geography and 17% use block groups. To understand location data, businesses must begin visualizing and analyzing at a deeper geographic level.

- Nearly all C-level and management level respondents,especially those from small to mid-sized organizations, note a strong likelihood to invest in Location

Intelligence within the next one (78%) to three years (84%). - Companies are very interested in finding data scientists that understand how to manipulate spatial data effectively, and conducting iterative spatial analysis is the most important step in applying Location Intelligence.

- “Ensuring data quality and accuracy” (49%), “gathering data real time” (40%), and “extracting data from existing systems in a usable way” (39%) are more commonplace challenges in terms of data collection.

Taking a closer look at these data, we can see for sure that if you know how to tap into the Location Intelligence right, your business can have a bright future and even expand, especially because many aren’t already using it at its full potential.

Therefore, how can you do more and be ahead of the rest? Entrepreneur.com is giving you some ideas:

- Use the big potential that research is offering you. “Location data can provide a stronger context of your target audience to better activate consumers. Beyond just marketing what you already have, it can also help reveal opportunities for products or services that you’ve not yet developed or marketed.”

- Competitive Intelligence. “This wealth of insight about where people go in the real world and, in particular, how they interact with your competition, is invaluable intelligence to your business and can help inform decisions about everything from pricing and inventory to in-store promotions and staffing levels.”

- Acquisition and investments. “Asset managers are increasingly turning to location data to inform their investments, according to a recent report from Optimas. Given this trend, location data should most definitely be part of your due diligence when evaluating any prospective investment or acquisition. Evaluate the foot traffic patterns in and around the business you’re considering and think about what it might reveal.”

More on the subject, tap here.

Inspirational study cases one can find in this Forbes article.

Contextual editorial video content in a video intelligence connected world

Contextual editorial video content dramatically increases a consumer’s engagement and recollection of video advertising on a web page, showed a new study about video intelligence, conducted by Lumen Research. The findings show an increase in dwell time by a third and improves user perception of publisher platforms by 9%.

In the study took part 200 consumers that were asked to share opinions on commercial and editorial content on an entertainment site, looking at engagement, dwell time and perception – both with and without contextual content. Respondents were invited to download Lumen’s software onto their laptop computers, which temporarily turns their computer’s webcam into an eye tracking camera. The participants eye movements were monitored to understand what they looked at – and what they ignored.

The findings showed an overwhelmingly positive reaction from when users are presented with contextual video content instead of standard advertising, or out-of-context video. Contextual content was shown to increase dwell time on the page by 33% – from 33 seconds to 47. The placement of video intelligence contextual content also saw an increase in the attention users paid to accompanying advertising, with 71% of respondents engaging with pre-roll video when viewed alongside contextual content, compared to just 50% when viewed without. Recollection of pre-roll was also increased as a result of the page featuring coherent contextual content.

Perception of publisher sites is improved with contextual video as a result of increased attention and engagement with content across the page. 85% of respondents described the page as engaging when viewed with contextual video (78% without), and 80% thought the entertainment site had ‘was enjoyable to browse’ when viewed with contextual video (69% without).

“We already knew contextual editorial content dramatically improves user engagement with advertising content, but to see that it improves engagement with other ad-content and native editorial content is fascinating. At video intelligence we’re dedicated to helping publishers deliver great user experiences, and we’re pleased to see that vi stories delivers a strong halo effect for both brand and publisher,” said Kai Henniges, CEO and co-founder of video intelligence.

On his turn, Mike Follett, managing director of Lumen Research, added that, because contextual content like video intelligence stories is more relevant and interesting than typical digital videos, people are willing to spend time with the accompanying advertising to see it, demonstrating that video intelligence stories makes both native content and non-contextual advertising on the same page more memorable. Attention matters – and vi drives attention.

vi stories allows publishers to embed a native video player on their platform that matches the look, style and design of their app or website. A natural language machine learning algorithm, powered by IBM Watson, finds and serves editorial video based on its analysis of the page content. Content is sourced from a vast and continually updating video library, containing clips from outlets like ITN, Bonnier and Euronews.

The product aims to create highly engaging experiences for users and increase the time they spend on the site, creating greater monetisation opportunities on publisher platforms. vi stories inserts advertising within the player, allowing advertisers to target engaged viewers with audience-appropriate branded content in a native media environment.

The research saw participants read an article on an entertainment website about the Oscars, half with contextually relevant video content and half without. The same ad for M&Ms ran before both videos. Having read the article and had the chance to watch the video, respondents were asked to complete a short questionnaire to assess their recall and perception of the ads they had seen and their perceptions of the publisher site. The respondents were paid for their time, and the software deleted from their machines as soon as the test was completed.

vi is a contextual video platform, connecting publishers, content providers and brands through video storytelling. Video inventory is lacking, and users are hard to captivate, therefor vi’s tools use contextual matching to create compelling video experiences on desktop and mobile. vi offers a full suite of self-serve tools: a video syndication engine powered by machine learning, a video ad server and an SSP. vi is trusted by 20,000 publishers to deliver millions of contextual video stories every day.

What Does It Take To Have Entrepreneurship In Your Blood

Is the entrepreneurial spirit something that you inherit or something you gain? Is it something that anyone can have or grow, or is it just for certain people? Can anyone become a successful entrepreneur or not? Those are a series of question that have been on many people’s mouths and minds during the years. Especially when confronted with the idea of starting a small business of their own.

A number of researchers, including Tim Spector and Lynn Cherkas of the Department of Twin Research and Genetic Epidemiology at Kings College, London, alongside Scott Shane, professor of entrepreneurial studies at Case Western Reserve University, studied the behavioral and molecular genetics of entrepreneurship by looking at a general pool of people, as well as identical and fraternal twins. They tested the number of businesses a person had started, the length of time someone was self-employed, and other factors such as the desire to run a business. According to inc.com, the findings included the following:

- 37 to 48 percent of the tendency to be an entrepreneur is genetic.

- The tendency to identify new business opportunities is in your genes.

- Self-employment income is heritable, which means that genetics affect not only the tendency to engage in entrepreneurship but also the ability to perform it.

- The tendency to have personality traits such as extroversion, openness, etc., has a genetic component. This suggests that your genes could affect your tendency to be an entrepreneur by influencing the type of personality you develop.

Another study, carried out by researchers from the UK universities of Birmingham and Reading on 17,000 children born in 1970, checking in with them again almost four decades later as they turned 38, found that the youngest children of parents who were not themselves self-employed were almost 50 per cent more likely to become entrepreneurs.

But when a family already had a business, things changed dramatically, the research showed. Last-borns were no more likely to be self-employed than their siblings. They were, in fact, 18% less likely to follow their parents into business – instead it was the first and middle children who had the highest propensity, at 151% and 118% respectively. Moreover, younger siblings were more “exploratory, unconventional and tolerant of risk”.

“Let’s face it – some people were born entrepreneurs stopping at nothing to pursue their passion to innovate and build extraordinary businesses.Failure is just another step in the process to success. Whether big fish – small pond or big fish – big pond – BIG is their goal,” said Randall Taussig.

Now, leaving aside all the researches and contemplation on the subject, if you really want to know if you are cut out to be an entrepreneur, I think you should take Gary Vaynerchuk’s advice:

If you want to know whether you’ve got that entrepreneurial spirit in your blood, here is what you do: You cut out watching your favorite sitcoms at night, you cut out playing more GTA5, you cut out going out for beers, you cut out being on the softball team, you pick a dream, and you attack it.

And if you prefer all that downtime over the upside of building your own business? I honestly think that’s great! That’s totally fine, but you’re not allowed to complain about how much you hate your job, just like I am not allowed to complain about my lack of free time or sleep.

How Luxury Marketing Will Look Like in 2018

The concept of luxury is changing, just like everything we are surrounded by is, like our preferences and sometimes passions. Consumer expectations of luxury continue to rise, and that what used to be luxury is now seen by the current generation of consumers, everyday experiences. And, as always, technology has a big part in this change as it makes everything easier,closer and more affordable, therefore what some years ago was considered luxury today might not be so. And just like what today is luxury in the years to come might not be anymore. The definition of luxury is changing, while “upper luxury” appears.

According to Deloitte’s “Global Powers of Luxury Goods 2018”, the world’s 100 largest luxury goods companies generated sales of US$217 billion in FY2016 and the average luxury goods annual sales for Top 100 companies is now US$2.2 billion. The report discusses the trends and issues that are driving the luxury industry. It also identifies the 100 largest luxury goods companies based on publicly available data for FY2016 (which they define as financial years ending within the 12 months to June 2017), and evaluates their performance across geographies and product sectors.

The growing importance of non-western markets for the luxury goods industry has been supported by supply chain leadership, technological innovation and international investment. These factors will help maintain further strong

growth in these geographical markets.

Deloitte’s “Global Powers of Luxury Goods 2018” points out:

Luxury brands have refocused their business strategies to capitalise on these changes. Giorgio Armani is engaged in an in-store installation collaboration agreement with Colombian artist Marta Luz Gutiérrez, while Louis Vuitton is conducting an advertising campaign using a

building designed by the late Mexican architect Luis Barragán. Rising prosperity in major cities and growing formal market power over the black market will ensure sustained Rest of the World (ROW) demand for luxury goods. To succeed in this context, luxury players should focus their investments on digital connectivity, upwardly mobile consumers and bold business models, which are key components of the

personal luxury industry today.

Some aspects that marketers must pay attention and act on in 2018:

Still according to Deloitte, collectively, Millennials and Generation Z will represent more than 40 per cent of the overall luxury goods market

by 2025, compared with around 30 per cent in 2016. Unlike Baby Boomers, many Millennial luxury consumers expect to interact with brands across a range of digital platforms, rather than only through traditional channels. Millennial consumers are also important for in-store shopping and expect a high-value, customized experience. Luxury brands should seek to change their business models to meet this demand, for example by providing more loyalty

programs and invitations to in-store events.

Customize your approach according to your audience. Personalization is still key as a marketing technique to be used as 45% of luxury consumers are asking for personalized products and services. With different expectations, younger

shoppers seek a personalized shopping experience that seamlessly integrates both online and offline platforms. This shift has motivated demand for connective technology such as Augmented Reality (AR) and Artificial Intelligence

(AI). By using AR and AI technologies, luxury brands can provide a personalized consumer experience, reach a wider audience, deepen product experience, and build stronger customer relationships. In parallel, the development of technologies such as voice commerce and the Internet of Things (IoT) are reshaping the entire luxury industry.

Luxury brands positioned as reliable sources of AI-driven recommendations are improving how they engage with consumers. More widespread adoption of AI is also making consumers increasingly reliant on suggestions and advice

provided by their various devices, rather than making decisions based on personal experience.

Social media becomes an important marketing tool for luxury as well. Instagram became the leading social media platform for fashion designers. Gucci more than doubled its Instagram followers between 2016 and March 2018, with successful Insta-campaigns such as #TFWGucci.

In future, the biggest challenge for luxury brands will be to make optimum use of social media without compromising their brand values. The success of a social media strategy will be converting “likes” into an interactive and engaging experience for customers.- Deloitte

An omnichannel approach – onnichannelluxury

A true omnichannel global market environment would require luxury brands to close gaps in customer experiences across channels, to offer a seamless, unified brand experience irrespective of the device or physical touchpoint used. Therefore, each channel needs to interact with and support

others to establish a single brand presence. Demand for an omnichannel approach is a natural development from the spread of digital technology and

e-commerce markets. During this process of change, the ability of luxury brands to leverage available inventory will be a key differentiator.

Digital must remain a priority to define an omnichannel strategy compatible with target expectations. The percentage of online sales perceived as being additional, and not a cannibalization of, physical sales is decreasing each year, with China the least cannibalized country to date.

“Luxury brands should develop their mobile strategy: 55% of luxury consumers buying online use their mobile phones versus personal computers. Peaks appear among the youngest generations and Chinese consumers, 75% and 77%, respectively, of whom use mobile. Social media and influencers are gaining power. For the first time, social media is the first source of information and the channel of primary impact used by true-luxury consumers, followed by magazines and brand websites. Five platforms (Facebook, Instagram, WeChat, Weibo, and QQ) are dominating the social media world, but Facebook is losing momentum to Instagram in the Western world and QQ is losing momentum to WeChat and Weibo in China,” states in “True-Luxury Global Consumer Insight”, the fifth edition of an annual study by The Boston Consulting Group (BCG) and Altagamma.

Millennials: Consumer Aspirations Are Disrupting Luxury

Collaborations with streetwear brands and artists are becoming the norm for Generation Zers and Millennials. “Collaboration covers demand for newness in a less risky way. It gives brands a cool edge and strengthens brand awareness as well as increases willingness to buy the brand. Collaboration is increasingly in demand and turns out to be a very effective purchasing incentive,” said Olivier Abtan, a partner in BCG’s Paris office and the global leader of the firm’s luxury, fashion, and beauty topic.

Unlike “absolute luxurers,” who buy luxury items exclusively, millennials do not hesitate to mix and match. According to BCG’s study, about 55% of this group trades down to buy handbags or T-shirts from cheaper brands, or mixes their style by buying sneakers and luxury shoes from luxury niche brands (including luxury sports). This trend appears to fulfill consumers’ need to create their own style. When they do look for different brands, it’s because luxury brands don’t have offerings in certain categories or because of the Millennials’ desire to have a unique style, express themselves, and seek out niche brands.

Use iconic personalities in your communication

With all the big changes, some things are meant to last and take the test of time. Chanel’s iconic marketing history began with a print advertisement for its perfume, Chanel No.5, in 1921. Its first celebrity endorsement didn’t feature until 1954, with Marilyn Monroe. However, it wasn’t until 2005 when Chanel first adopted videography, and from here, the rest is history.

“Despite not adopting social media and integrating the platform with videography until 2009, its marketing strategy is nothing short of stupendous. Selecting admirable public figures such as Keira Knightley and Nicole Kidman to star in Chanel’s unmistakable short films, revived the brand as an iconic symbol of both cultural and digital relevance. With the use of video and social media integration, Chanel has grown to having more than 57 million social followers globally, the highest in the luxury fashion industry. The brand focused on Facebook as their initial social media platform, due to the video capabilities such as extended video length, that Twitter and Instagram do not support. For the brand’s primary consumer, the more wealthy and mature client, Facebook was the ideal platform for accessing this demographic,” wrote Little Agency.

Sensory Branding

According to Retail Insider, British Airways is encashing big on a recent study on sensory sciences by Oxford about how sound influences the taste of food. Based on the findings of this study, they launched a list of 13 in-flight tracks to enhance the taste of the meals served during the flight, providing a truly luxurious experience. Moreover, Soundwich in Portugal delivered gourmet sandwiches packed in metal boxes that play music chosen by the chef when opened.

More ideas you can see here.

Nomophobia – what it is and how it presents itself

95 percent of Romanians don’t leave the house without their smartphone. This is only one of the information gathered by Huawei, that conducted a study together with the multinational market research company Ipsos, collecting data from 12 countries, including Romania. The purpose of the study was to analyse the behaviour of smartphone users over 24 hours.

The study by Huawei and Ipsos concludes that 79 percent of Romanians use their smartphone to read their e-mails, check their social media accounts and messages, while 64 percent do this when they wake up. This is one of the reasons why 60 percent of Romanians take their phones to bed with them and around 11 percent admit that they sleep with their phone next to them.

Huawei also conducted a survey called “Smart relationships” to analyse the average “relationship” each user has with their smartphone. The results show that 59 percent of Romanians check their phones several times per hour, and their habit includes searching for information, using the device for entertainment, navigating social media networks or the internet, reading news and connecting to their home bank systems. Thus, the research evidently shows how “attached” Romanians are to their smartphones.

The study also showed that 87 percent of Romanians need a smartphone to send text messages, 72 percent use it to capture photographs and, of course, 79 percent use it to check social media networks. It was also found that 56 percent of respondents admit that they keep their smartphones with them for over 13 hours a day, while 27 percent actively use the smartphone for 3-4 hours/day. The places where Romanians use their phones the most are: 66 percent while being in the kitchen and 47 percent when they’re in their children’s rooms.

This situation of mobile dependency already has a name: nomophobia. “”NO MObile PHOne phoBIA” is a 21st-century term for the fear of not being able to use your cell phone or other smart device. Cell phone addiction is on the rise, surveys show, and a new study released Thursday adds to a growing body of evidence that smartphone and internet addiction is harming our minds,” wrote CNN.

According to The Guardian, when Deloitte surveyed 4,150 British adults in 2017 about their mobile habits, 38 percent said they thought they were using their smartphone too much. Among 16- to 24-year-olds, that rose to more than half. Habits such as checking apps in the hour before we go to sleep (79 percent of us do this, according to the study) or within 15 minutes of waking up (55 percent) may be taking their toll on our mental health.

“It’s not necessarily the top thing when my clients come in, but it’s often in the mix, tied in with anxiety or insomnia or relationship issues. Particularly when anxiety and insomnia’s there, it’s rare that it’s not related in some way to heavy use of digital devices,” said psychotherapist Hilda Burke, a spokesperson for National Unplugging Day in 2016 and 2017.

Moreover, a small study presented at the annual meeting of the Radiological Society of North America in Chicago showed that cell phone addiction may affect brain functioning.”Researchers from Korea University in Seoul used brain imaging to study the brains of 19 teenage boys who were diagnosed with internet or smartphone addiction. Compared with 19 teenagers who were not addicted, the brains of the addicted boys had significantly higher levels of GABA, a neurotransmitter in the cortex that inhibits neurons, than levels of glutamate-glutamine, a neurotransmitter that energizes brain signals,” added CNN.

How to inspire innovation in your employees

According to McKinsey & Company and its global innovation survey, innovation is critical to growth, particularly as the speed of business cycles continues to increase. Most companies understand the importance of innovation, but fall short when it comes to execution. “We define innovation as creativity plus delivery, helping our clients transform their innovation performance by focusing on four requirements for innovating at scale: strategy, pipeline of ideas, execution, and organization.”

Following a multiyear study comprising in-depth interviews, workshops, and surveys of more than 2,500 executives in over 300 companies, including both performance leaders and laggards, in a broad set of industries and countries, the company discovered the ingredients that lead to innovation.

Since innovation is a complex, company-wide endeavor, it requires a set of crosscutting practices and processes to structure, organize, and encourage it. The first four, which are strategic and creative in nature, help set and prioritize the terms and conditions under which innovation is more likely to thrive. The next four essentials deal with how to deliver and organize for innovation repeatedly over time and with enough value to contribute meaningfully to overall performance.

Who are those essentials? Aspire,Choose, Discover,Evolve,Accelerate, Scale, Extend, Mobilize.

Even there is no proven formula for success, particularly when it comes to innovation, McKinsey & Company’s representatives firmly believe that if companies assimilate and apply these essentials—in their own way, in accordance with their particular context, capabilities, organizational culture, and appetite for risk—they will improve the likelihood that they, too, can rekindle the lost spark of innovation. In the digital age, the pace of change has gone into hyperspeed, so companies must get these strategic, creative, executional, and organizational factors right to innovate successfully.

One can read more on the subject here.

How this transfer to the employees? According to Forbes, there are three tools that can inspire innovation to the employees: giving employees the permission to learn, motivating people to go places they wouldn’t otherwise go and sharing experiences across management lines. “Asking employees to keep a Best Practice Journal is another way to inspire employees to learn by observing what’s happening around them. Ask your people to document examples of great performance as they see it happening out in the world and make time for sharing these observations at regular staff meetings,” added Mark Murphy for Forbes.

Another set of great ideas may be found here.

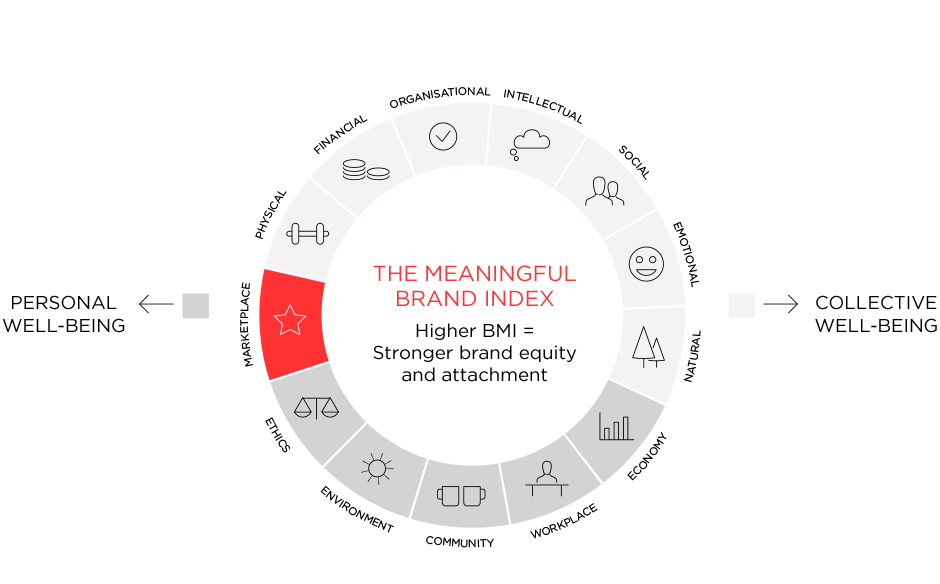

What is a meaningful brand?

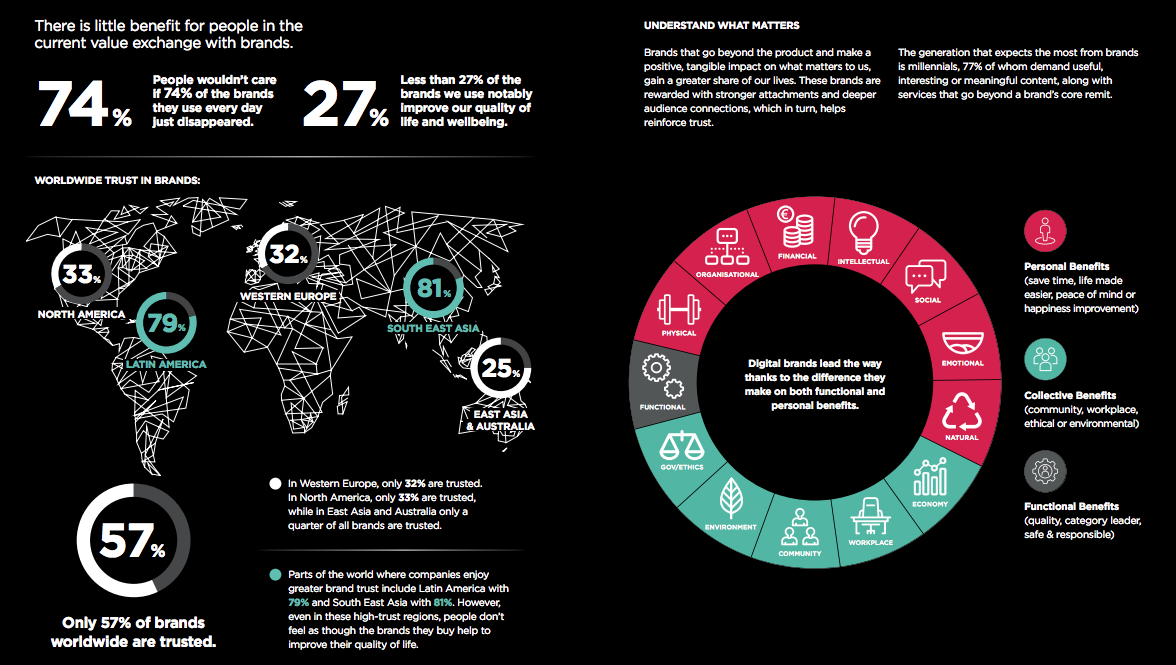

60% of the content created by the world’s leading 1,500 brands is “just clutter” that has little impact on consumers’ lives or business results, by being poor, irrelevant or failing to deliver, showed a report by media agency Havas, quoted by Media Week UK. The ‘Meaningful Brands’ study looked at the role of content and it questioned 375,000 people across 33 countries. Furthermore, the study found that 84% of the respondents expect brands to produce content,that can range from digital content such as podcasts or a web series to experiential events.

“Driven by their increased interconnectivity, audiences have now become media

platforms in their own right. It’s now more important than ever to effectively engage these audiences so that they will propel your brand’s values, messages and drive loyalty, recommendation and ultimately, sales. We also live in a world of content overload. A world where every day 500 million tweets, 4.3 billion Facebook messages and 500 million hours of YouTube footage are sent, posted and uploaded. In this world, only brands that form more meaningful connections with people will prosper. Brands need to know why people care, and what makes their brands meaningful,” said Yannick Bolloré, Chairman and CEO, Havas Group.

The shocking news is that, according to the study, the respondents declared that they wouldn’t care if 74% of the brands they are using daily would disappear and that less than 27% percent of the brands that exist are improve our quality of life and wellbeing.

But what does a meaningful brand stand for? According to Havas’ results, a meaningful brand is defined by its impact on our personal and collective wellbeing, plus its functional benefits. Content’s role is to educate, inform, entertain, inspire, reward and help,while great content is a great driver of personal wellbeing and therefore meaningfulness.

More about the study and how your brand can reach meaningfulness, one can read here.

How relevant is still TV for your brand?

We are smarter and smarter consumers, more up-to-date with everything that is new and happening in the world of technology, people constantly changing and improving their laptops, mobile phones and software that they are using. Moreover, 2017 proves to be the first year that the media investments in digital are surpassing the TV ones. In this context, it’s only natural for a CEO or a marketing specialist to wonder how relevant is still TV for the brand they are taking care of?

In other words is video killing the radio star? Or is it a non-subject that the specialists are over-exaggerating talking about? What do you think? Well, this is what we think.

First of all we believe that there is not a general answer of yes or no. The right answer for your brand will come from your target: who are they, what are their consumption preferences, their passions, hobbies, desires, etc. Better knowing your target will give you the right answer. Because if you are looking at the younger generation the answer is pretty easy, but if you are targeting the Millennials or the older generation you will have for sure another look at the situation and things will not seem that much black and white.

Along with the channels and devices available for watching TV, the ways for brands to reach consumers through the medium are proliferating. Quoted by Marketing Week, Otto Rosenberger, CMO at Hostelworld.com, believes that TV buying is changing, and with good reason. He says: “It really always starts with being obsessed about where the customer is. It’s about where they are and what drives them, which drives our creative and media decisions.” Research released by Ofcom earlier this month shows that while live television remains hugely important, catch-up TV viewed via the internet and programming premiered online are taking up an increasing share of viewing time for younger audiences in particular. It reveals that today, only 50% of 16- to 24-year-olds’ TV consumption is through live television, rising to 61% for 25-to 34-year-olds.

“The overarching shift, therefore, is in the power of technology and the internet. It is not only changing the way people watch TV, it is also creating a significant change in the way TV advertising is being traded towards targeting specific segments of audiences known to be watching rather than programmes that research panel data suggests they might see,” explains Marketing Week.

Not a long time ago, Turner Broadcasting and Horizon Media partnered on with marketing-analytics company MarketShare, which meta-analyzed thousands of marketing optimizations used by major advertisers from 2009 to 2014. MarketShare’s analysis found that TV advertising effectiveness has remained steady during that time period and outperforms digital and offline channels at driving key performance metrics like sales and new accounts. The study also showed that networks’ premium digital video delivered higher than average returns when compared with short-form video content from non-premium publishers. More on the main results you can read here.

Moreover, we need to think about the fact that a deep investigation of the decision journey often reveals the need for a plan that will make the customer’s experience coherent—and may extend the boundaries of the brand itself. The details of a customer experience plan will vary according to the company’s products, target segments, campaign strategy, and media mix. But when the plan is well executed, consumers’ perception of the brand will include everything from discussions in social media to the in-store shopping experience to continued interactions with the company and the retailer.

“Consumers’ perception of a brand during the decision journey has always been important, but the phenomenal reach, speed, and interactivity of digital touch points makes close attention to the brand experience essential—and requires an executive-level steward. At many start-ups the founder brings to this role the needed vision and the power to enforce it. Established enterprises should have a steward as well. Now is the time for CMOs to seize this opportunity to take on a leadership role, establishing a stronger position in the executive suite and making consumers’ brand experience central to enterprise strategy,” said David C. Edelman for Harvard Business Review.

A study done by Arris showed that 84% of respondents wanted to fast forward through the ads they watch, while 60% of them download or record shows so they can skip commercials. Even Super Bowl ads have lost their effectiveness: a 2014 study showed that 80% of them do not increase sales for the companies running them. The increased use of smartphones and tablets also detracts from TV commercials’ relevance. A study in May 2015, quoted by The Guardian, showed that researchers found that viewers who focused just on the TV screen were able to recall 2.43 out of every three brands mentioned, while smartphone and tablet users only managed to recall 1.62 on average.

Moreover, advertising’s even losing its role as an information source: a study by Mindshare earlier in 2015 showed that the percentage of Americans who said advertising helped them learn about products and services dropped from 52% in 2005 to 41% in 2014.

Still, all in all, TV is still relevant and will still be as long as the brands will know how to adapt to the new changes it brings and will know how to showcase its added value. As long as the TV advertising will continue to adapt and become better and more relevant for its audience, it will of course remain very important.

On how brands can optimize their TVCs to drive product discovery, you can read here.

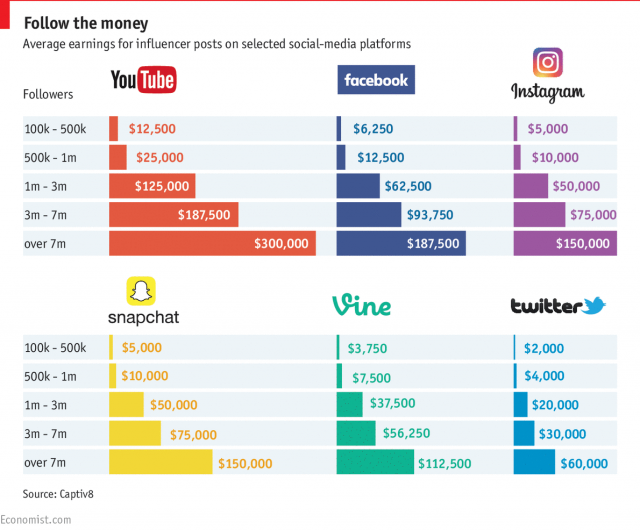

Big influencers attract thousands of dollars for just a post on social media

Only 3% of the marketers said they planned to cut back on influencer marketing in the coming year, versus about 75% who anticipated spending even more on it, says emarketer.com. Moreover, according to the website, companies are paying the most for celebrity posts, especially on certain platforms. On average, posts by celebrities with at least 1 million followers (considered as influencers) cost nearly £65,000 each ($87,731), with Facebook posts demanding a leading rate of approximately £75,000 ($101,228).

Influencer marketing costs are going up in the UK, according to research by Rakuten Marketing and Morar Consulting, but prices per post vary considerably depending on reach and platform. This month, polling of UK marketers working directly on influencer programs from sectors including fashion, beauty and travel, approximately two-thirds of respondents had seen the prices influencers charge for posts go up in the past 12 months. In some industries, the costs were even higher, with some premium fashion brands, for example, paying celebrity influencers more than £160,000 ($215,954) per post.

“UK marketers are willing to pay celebrity influencers on Facebook up to £75,000 for a single post mentioning the brand they want to promote, a new survey has revealed. They are also prepared to pay celebrity influencers £67,000 for each YouTube video that mentions their brand, while key influencers on Snapchat can expect to be paid as much as £53,000 per Snap,” writes www.warc.com.

Spending was much more modest for so-called micro-influencers—those with 10,000 or fewer followers, due to the fact that only a fifth (20%) of marketers claim they are able to demonstrate the impact of influencers through indirectly influenced sales. Prices averaged at close to £1,350 ($1,822) per post, with YouTube and Facebook commanding the highest prices—more than £1,500 ($2,025)—and Snapchat the lowest at just over £1,000 ($1,350).

“Decision makers questioned from across a variety of sectors including fashion, FMCG, beauty and travel admitted that they would shell out as much as £53,000 per Snapchat post, which despite coming in at significantly less than the value they placed on other platforms, is notable given that Snapchat’s ephemeral nature means videos and pictures disappear within 24 hours of being posted,” said Rebecca Stewart for thedrum.com.

Overall, respondents said they would devote an average of 24% of their marketing budgets to influencer marketing in the next 12 months. That figure’s higher than the share of budgets that the largest percentage of marketers in the UK and US said they devoted to influencer marketing in a March 2017 study by Econsultancy. In that study, between half and six in 10 luxury and non luxury brand marketers said they invested less than 10% of their overall marketing budgets to influencer marketing. But the second largest shares of respondents were similar in their spending allotment to those in the Rakuten and Morar study.

Affiliate marketing firm Rakuten Marketing spoke to 200 UK marketers working on influencer programmes and found that post-for-post they were prepared to pay 12% more for Facebook endorsements than they were for YouTube. The research also found that despite the value brands clearly place on high-profile influencer slots, the majority of those asked (86%) admit they aren’t entirely sure how influencer fees are calculated. Which is pretty odd, especially after the last years of change in the media buying market, the restriction of budgets and the overall risen caution.

Why are the influencers so important for marketers when it comes to social media? According to The Economist, social media offer brands their best opportunity to reach cord-cutting millennials: Snapchat, for instance, reaches 40% of all American 18- to 34-year-olds every day.

“Moreover, these platforms can make consumers feel they have gained unprecedented access to the lives of the rich and famous. That lets sponsors interact with their target audiences in ways that traditional advertising cannot match. In turn, demand from marketers for these channels has made social media lucrative territory for people with large online followings,” wrote the famous business magazine.

On the other hand, while 59 per cent of marketers state the influencers they work with will take guidance from them around best practice, 56 per cent of premium fashion marketers admit to a situation in which influencers hold all of the power. For example, only 20 per cent of marketers state influencers are prepared to follow their lead when it comes to guidance around billing.

Less than a third (29 per cent) believe that the influencers they work with are entirely concerned whether their content drives sales for the brand. Interestingly, when asked what would encourage marketers to invest more in an influencer programme, greater transparency and better reporting of influencer contribution to sales now rank as the highest factor (50 per cent).

James Collins, Rakuten Marketing’s SVP/managing director, global attribution, comments, “Influencer marketing can be hugely effective but marketers are commissioning expensive posts without understanding the real impact on the purchase journey. It’s essential that marketers question influencer fees and use attribution tools to measure the effect of this activity in order to create strong, value-driven relationships between brands and influencers.”

Batteries, solar panels and the end of fossil fuels

A study published in January in the Journal of Sustainable Finance & Investment predicts that the combination of battery storage with renewable energy will make fossil fuels increasingly obsolete. The driving forces of this disruption include the “decline in retail renewable electricity prices,” along with plummeting costs of batteries. Fossil fuels are the most widely used source of energy because of base load power, which means they provide energy at all times, night and day. In contrast, renewables have faced the ‘intermittency’ challenge—the sun doesn’t always shine, and the wind doesn’t always blow.

But authors Jemma Green and Peter Newman of Curtin University in Australia show that as storage gets cheaper, renewables will become more competitive with fossil fuels on costs and reliability. By 2050, these irresistible technological and market forces could make oil, gas and coal seem too costly and cumbersome, leading renewables to account for “100 percent of global energy demand.”

![]()

source: energyathaas.com

According to Vicente Lopez-Ibor Mayor, chairman of Lightsource—the biggest solar energy company in Europe—there will be an immediate impact within just three years. Moreover, Mayor told Motherboard that the speed of technological improvement means solar storage is “going to be massively disruptive to the business-as-usual processes of oil, gas and coal.”

In three years, he said, it will “begin to transform” the electricity infrastructure of major cities. “Solar storage is pitched to become so cheap it will make relying on natural gas peaker plants pointless…It will lead to rapid adoption of solar by businesses, local governments, and households—not because people are environmentally conscious, but simply because it will make more economic sense.”

More on their approach you can read here.

The Powerwall system

While wind and solar power have made great strides in recent years, with renewables now accounting for 22% of electric energy generated, the issue that has held them back has been their transience. But now, the renewable power billionaire Elon Musk has just blown away that final defence. In an event held in California he introduced to the world his sleek new Powerwall – a wall-mounted energy storage unit that can hold 10 kilowatt hours of electric energy, and deliver it at an average of 2 kilowatts, all for US 3,500. That represents an electricity price (taking into account installation costs and inverters) of around US 500 per kWh – less than half current costs, as estimated by Deutsche Bank.

“That translates into delivered energy at around 6 cents per kWh for the householder, meaning that a domestic system plus storage would still come out ahead of coal-fired power delivered through the conventional grid,” explains iflscience.com.

Moreover, the reality is much closer than we might think as Musk is going to manufacture the batteries in the United States, at the “gigafactory” he is building just over the border from California in Nevada. And that while not staying and waiting for some totally new technology, but scaling up the tried and tested lithium-ion battery that he is already using for his electric vehicles.

The Powerwall system offering 10 kWh is targeted at domestic users. It is complemented by a commercial system termed the Powerpack offering 100 kWh storage, and a stack of 100 such units to form a 10 megawatt hour storage unit that can be used at the scale of small electricity grids. Whole communities could build micro-grid power supply systems around such a 10 MWh energy storage system, fed by renewable energy generation (wind power or rooftop solar power), at costs that just became super-competitive.

More than that, Musk declared that the entire electric power grid of the US could be replicated with just 160 million of these utility-scale energy storage units. And two billion of the utility-scale units could provide storage of 20 trillion kWh – electric power for the world.

Solar panels have repaid their fossil fuel debt

At the same time, another study says that thanks to the growing solar power capacity around the world, solar power has reached the break even point. The study from the Netherlands, published in Nature Communications, says that the power generated by solar photovoltaic panels over the last 40 years has offset the polluting energy used to produce them.

By the researchers’ calculations, for every doubling of global solar power capacity, the energy used to produce them fell by 12-13 percent and greenhouse gas emissions fell by 17-24 percent, depending on what material was used. Solar capacity has grown roughly 45 percent a year since 1975, reaching 230 gigawatts (GW) in 2015. By the end of 2016, there could be 300 GW installed.

“The researchers believe the break even point was likely hit about five years ago for both energy consumed and emissions meaning, at this point, global solar energy is having a net positive impact and will continue to increase that positive impact going forward. This feels like a major cause for celebration. If you’re a homeowner with solar panels, the researchers say that individual solar panels repay their fossil fuel debt several times over during their average 30-year lifespan,” wrote Megan Treacy for treehugger.com.

The best local brands that went global

The world’s largest brands are facing a dual threat from slowing growth in developed economies and the rising popularity of homegrown brands. As getting more sales from existing customers becomes increasingly difficult, and costly, brands are turning their attention to the places where they can attract new customers – emerging markets. According to Kantar Worldpanel’s fifth annual Brand Footprint study, emerging markets now account for 51% of global spend on fast-moving-consumer-goods (FMCG), up from 48% just three years ago. Emerging countries added $34 billion to the global industry throughout the year, a gain of more than 6% over last year, while sales in developed markets were flat. This year’s ranking analyzed 15,300 brands and 1 billion households in 43 countries across five continents in the 12 months to November 2016.

Looking to go global? Join this masterclass!

“The underlying theme of this year’s report is disruption,” said Josep Montserrat, chief executive officer of Kantar Worldpanel. “This not only relates to the political and economic climate of today, but also to the increasing number of disruptor brands and trends which are upsetting the status quo.”

While global brands remain dominant, local brands are achieving faster growth. Local brands grew by 3.9% in 2016, compared with 2.6% growth for global brands.

“In 2016, the price gap between global and local brands has narrowed to the point of disappearing,” said the report. “No longer does being a global brand automatically command a price premium. Global brand owners are having to work harder to convince consumer that a global choice offers the additional reassurance of quality and confers prestige.”

Local brands claimed the top spot in more than half of the countries studied by Brand Footprint. Some of these brands represent a more affordable option in struggling economies like Brazil and Argentina. However, in developed markets consumers have shown they are willing to pay a premium for homegrown products. Local brands are seeing the strongest performance in the food and beverage categories, while health and beauty brands continue to be driven by global brands.

Becoming a successful global brand requires an understanding of local cultures, lifestyles and ideologies, according to two industry figures. In a WARC Best Practice paper, How global brands resonate across cultures, Sue Mizera and Alessandra Cotugno, senior executives at Young & Rubicam, observe that the standardization of brand name, logo, image, packaging and brand positioning simply enables brand recognition in multiple markets. Moreover, different brand values emerge as more important in different countries: Germans like the notion of directness, for example, while Indonesians prefer kindness and South Koreans favor energetic brands.

Here are five great local brands that are worldwide global successes:

- IKEA

In the 1980s, IKEA expands dramatically into new markets such as USA, Italy, France and the UK., the brand beginning to take the form of today’s modern IKEA. In the 2000s, IKEA expands into even more markets such as Japan and Russia. This period also sees the successes of several partnerships regarding social and environmental projects. Today is a major retail experience in 40 countries/territories around the world.

Marcus and Sam commissioned a fleet of steamers to carry oil in bulk, using for the first time the Suez Canal. They also set up bulk oil storage at ports in the Far East and contracted with Bnito, a Russian group of producers controlled by the Rothschilds, for the long-term supply of kerosene.

Their strategy was high-risk: if news of their operations got out they would be squeezed out by Rockefeller’s dominant Standard Oil. With the maiden voyage of the first bulk tanker, the “Murex”, through the Suez Canal in 1892 the Samuels had achieved a revolution in oil transportation. Bulk transport substantially cut the cost of oil by enormously increasing the volume that could be carried. The Samuel brothers initially called their company The Tank Syndicate but in 1897 renamed it the Shell Transport and Trading Company.

In 1907 the company merged with Royal Dutch Petroleum Company, becoming The Royal Dutch Shell Group. There were two separate holding companies with Royal Dutch taking 60% of earnings and Shell Transport taking 40%. The business was run by a variety of operating companies. The merger transformed the fortunes of both companies. Under the management of Henry Deterding they turned from struggling entities to successful enterprises within twelve months.

The Group rapidly expanded across the world. Marketing companies were formed throughout Europe and in many parts of Asia. Exploration and production began in Russia, Romania, Venezuela, Mexico and the United States. The first twelve years also provided many exciting opportunities to demonstrate the quality of the products in the new, fast-developing market for gasoline. These included record-breaking races, flights and journeys of exploration.

More on the history you can read here.

3. Nestlé

The company history begins in 1866, with the foundation of the Anglo-Swiss Condensed Milk Company. Henri Nestlé develops a breakthrough infant food in 1867 and in 1905 the company he founded merges with Anglo-Swiss, to form what is now known as the Nestlé Group. During this period cities grow and railways and steamships bring down commodity costs, spurring international trade in consumer goods. In 1904, Nestlé begins selling chocolate for the first time when it takes over export sales for Peter & Kohler. Henri Nestlé himself plays a key role in the development of milk chocolate from 1875, when he supplies his Vevey neighbour Daniel Peter with condensed milk, which Peter uses to develop the first such commercial product in the 1880s.

In 1960, with increasing numbers of households buying freezers, demand for ice cream is rising. Nestlé buys German producer Jopa and French manufacture Heudebert-Gervais to capitalise on this growth, and adds Swiss brand Frisco in 1962. The company also buys UK canned foods company Crosse & Blackwell. In 1961, Nestlé buys the Findus frozen food brand from Swedish manufacturer Marabou, and extends the brand to international markets. Findus is one of the first companies to sell frozen foods in Europe, from 1945. As chilled dairy products are increasingly popular, Nestlé buys French yogurt producer Chambourcy. In the early 1970s the latter launches the Sveltesse range of yoghurts, aimed at health- and weight-conscious consumers.

Moreover, 1969 is the year the company enters on the mineral waters market by buying a stake in French waters brand Vittel.

In 1974, for the first time, Nestlé diversifies beyond food and drink, becoming a minority shareholder in global cosmetics company L’Oréal. Three years later,the renamed Nestlé S.A continues its diversification strategy by buying US pharmaceutical and ophthalmic products manufacturer Alcon Laboratories.

More on the company’s expansion you can read here.

4. Carlsberg

The brand was born in 1847, but the international approval came just 21 years later when the first Carlsberg beer was exported to Great Britain. Carlsberg was founded by J. C. Jacobsen, a philanthropist and avid art collector. With his fortune he amassed an impressive art collection which is now housed in the Ny Carlsberg Glyptotek in central Copenhagen. The first brew was finished on 10 November 1847, and the export of Carlsberg beer began in 1868 with the export of one barrel to Edinburgh, Scotland.

The first overseas license for brewing was given to the Photos Photiades Breweries, and in 1966 Carlsberg glass and beer was brewed for the first time outside Denmark at the Photiades breweries in Cyprus. The first brewery to be built outside Denmark was in Blantyre, Malawi in 1968.

Carlsberg merged with Tuborg breweries in 1970 forming the United Breweries AS, and merged with Tetley in 1992. Carlsberg became the sole owner of Carlsberg-Tetley in 1997. In 2008, together with Heineken, it bought Scottish & Newcastle, the largest brewer in the UK, for £7.8bn ($15.3bn). In November 2014, Carlsberg agreed to take over Greece’s third largest brewery, the Olympic Brewery, adding to its operations in the country already and effectively transforming the firm into the second biggest market player in Greece.

More about the company’s growth you can read here and here.

5. Mercedes

The brand is known for luxury vehicles, buses, coaches, and trucks. The headquarters is in Stuttgart, Baden-Württemberg. The name first appeared in 1926 under Daimler-Benz. Mercedes-Benz traces its origins to Daimler-Motoren-Gesellschaft‘s 1901 Mercedes and Karl Benz’s 1886 Benz Patent-Motorwagen, which is widely regarded as the first gasoline-powered automobile.

Mercedes-Benz traces its origins to Karl Benz‘s creation of the first petrol-powered car, the Benz Patent Motorwagen, financed by Bertha Benz and patented in January 1886, [3] and Gottlieb Daimler and engineer Wilhelm Maybach’s conversion of a stagecoach by the addition of a petrol engine later that year. The Mercedes automobile was first marketed in 1901 by Daimler-Motoren-Gesellschaft. (Daimler Motors Corporation).

Emil Jellinek, an Austrian automobile entrepreneur who worked with DMG created the trademark in 1902, naming the 1901 Mercedes 35 hp after his daughter Mercedes Jellinek. The first Mercedes-Benz brand name vehicles were produced in 1926, following the merger of Karl Benz’s and Gottlieb Daimler’s companies into the Daimler-Benz company. On 28 June 1926, Mercedes Benz was formed with the merger of Karl Benz and Gottlieb Daimler’s two companies.Throughout the 1930s, Mercedes-Benz produced the 770 model, a car that was popular during Germany’s Nazi period. Adolf Hitler was known to have driven these cars during his time in power, with bulletproof windshields. The pontiff’s Popemobile has often been sourced from Mercedes-Benz.

More you can read here.

Some of Romania’s most successful and famous brands at an international level are: Dacia, Aqua Carpatica, ROM, Ursus, Bitdifender, Farmec, etc.